Mastering RA Billing Preparation in Construction: A Complete, Step-by-Step Guide for Contractors

How to prepare a Running Account bill that gets approved the first time, every time

Why I Decided to Write This Guide ?

Anyone who has spent real time on the RA billing preparation side of a construction project knows a simple truth: billing is not paperwork, it is the lifeline of the project. Everything else on site labour payments, material purchases, subcontractor dues, overheads, even the contractor’s own survival depends on one thing happening correctly and on time: the RA bill getting certified and paid.

I have sat on both sides of this process preparing bills as a contractor’s billing engineer, and reviewing bills as part of a client’s project team. And if there is one lesson that gets repeated project after project, it is this: most payment delays are not caused by the client being difficult. They are caused by an incomplete or inconsistent bill.

A missing measurement reference, a rate that doesn’t match the work order, a GST figure that doesn’t tie back to the abstract, an invoice number that has a typo any one of these can push a payment back by weeks. Multiply that delay across ten RA bills over the life of a project, and you are looking at a serious cash flow problem, not just an administrative headache.

This guide is my attempt to put down, in one place, everything I know about preparing a Running Account (RA) bill from the very first document you should collect before opening Excel, right down to the checklist you tick just before you hit “send.” I have also built a ready-to-use Excel template (linked at the end of this article) that mirrors every sheet described here, so you can start using this system on your very next bill instead of just reading about it.

I have written this the way I would explain it to a new billing engineer joining my team slowly, with the reasoning behind each step, and with the mistakes I have personally seen (and made) along the way. Whether you are a contractor’s billing executive, a project accountant, a site engineer who has been asked to “just prepare the bill this month,” or a client-side quantity surveyor checking incoming bills, I hope this becomes something you keep coming back to.

Understanding What RA Billing Actually Is

1.1 What “Running Account” Means

In a construction contract, the contractor does not get paid only once the entire project is finished. That would be impractical nobody can fund months or years of labour, material, and equipment cost out of pocket while waiting for a single final payment. Instead, the contract allows the contractor to bill the client periodically usually monthly for the work that has actually been executed and measured up to that point.

This periodic bill is called a Running Account bill, or RA bill. Each RA bill represents:

- The work done since the last bill (the “current” quantity and amount)

- The cumulative work done since the start of the contract (used to check against the total contract value)

- Any deductions applicable as per the contract (tax deducted at source, retention money, mobilisation advance recovery, and so on)

The word “running” is important. It tells you that the bill is not a one-time, isolated document it is part of a continuous, cumulative record that runs alongside the project from the first bill to the final bill. Every RA bill must reconcile with the one before it. If RA-03 shows a cumulative quantity that doesn’t logically follow from RA-02, you have a problem before the client even opens the file.

1.2 Why Billing Is Not “Just Filling an Excel Sheet”

I want to be very direct about something early in this guide: billing is a technical, contractual, and financial exercise all at once. It sits at the intersection of three different disciplines, and a good billing engineer needs to think like all three:

- The engineer — because you are certifying that a certain quantity of work has physically been executed at site, matching drawings, specifications, and the measurement book.

- The contract manager — because the rates, terms, deductions, and escalation clauses you apply must come directly from the signed Work Order, not from memory or from what “seems fair.”

- The accountant — because GST, TDS, retention, and net payable calculations must be arithmetically perfect and must match the tax invoice raised alongside the bill.

If any one of these three lenses is missing, the bill will eventually run into trouble either at the client’s desk during certification, or later during an internal or statutory audit.

1.3 The Real Cost of Getting It Wrong

I have seen the following consequences play out on real projects, and they are worth listing plainly so the stakes are clear:

- Payment delays — a single mismatched figure between the invoice and the abstract can put an entire bill on hold, sometimes for the whole payment cycle (30, 45, or 60 days), because clients often refuse partial certification.

- Financial losses — undercharging due to a wrong rate, a missed item, or a quantity that wasn’t captured properly means that money is simply left on the table and, in many contracts, cannot be recovered later.

- Disputes — if two bills disagree on cumulative quantity, or if a reconciliation was never done, the client and contractor can end up arguing over numbers instead of discussing the project.

- Audit objections — whether it is an internal audit, a statutory GST audit, or a client’s post-project reconciliation, an incomplete billing trail (missing MB references, no maker-checker sign-off, no version control) is exactly what auditors flag.

None of these outcomes are inevitable. They are almost always the result of a billing process that was never standardised where every bill is prepared slightly differently, by whoever is free that week, with no fixed template and no fixed checklist. The rest of this guide exists to fix precisely that.

The Anatomy of a Complete Billing Submission

Before you open a single Excel sheet, it helps to know what a complete RA bill package actually contains. I think of it as five layers, each one built on the layer below it.

Layer 1 — The Contract Base

This is the foundation everything else rests on. It includes:

- The signed Work Order or Letter of Intent (LOI), which defines the legal relationship

- The approved Bill of Quantities (BOQ) — the master list of items, units, and rates

- The payment terms — credit period, milestone conditions, escalation clauses if any

If you do not have an up-to-date, signed version of these three documents in front of you, stop right there. Nothing you calculate afterwards can be trusted until the base is correct.

Layer 2 — Execution Proof

This layer answers the question: how do we know the work was actually done?

- The Measurement Sheet, drawn from the Measurement Book (MB) maintained at site

- Work-done intimations — the formal notice a contractor gives when a portion of work is ready for measurement/inspection

- Quantity backup — photographs, drawings marked up with measured areas, joint measurement records signed by both contractor and client representatives

Layer 3 — Financial Calculation

This is where engineering quantities are converted into money.

- The BOQ Billing Sheet, applying contract rates to measured quantities

- The Abstract Sheet, summarising previous, current, and cumulative billing

- The Top Sheet, which is the final financial summary the client actually signs off on

Layer 4 — Commercial Documents

- The Tax Invoice, which must mirror the Abstract and Top Sheet exactly

- GST compliance documents — HSN/SAC codes, applicable GST rate, e-invoice details if applicable

Layer 5 — Validation System

- A Checklist confirming every document above is present and correct

- Internal approvals — typically a “maker” who prepares the bill and a “checker” who reviews it before it leaves the office

I want to underline one point here, because it is the single most common reason bills get rejected or delayed: if even one component from these five layers is missing, you have created rejection risk. A perfect BOQ Billing Sheet with no matching tax invoice is not a complete bill. A beautifully formatted Top Sheet with no measurement backup behind it is not a complete bill. Completeness, not polish, is what gets a bill certified quickly.

The Step-by-Step Process of RA Bill Preparation

This is the heart of the guide. I have broken the process into nine steps. I strongly recommend following them in this order skipping ahead (for example, jumping straight into the BOQ Billing Sheet before finishing the Measurement Sheet) is exactly how errors creep in.

Step 1: Work Order Analysis

Before you touch Excel, you need to sit with the Work Order and BOQ and genuinely understand what you are billing against. Do not assume you remember the terms from the last project every contract is different, and small clause differences change how you must bill.

Specifically, confirm:

- Scope of work — what exactly is included, and just as importantly, what is explicitly excluded

- Unit of measurement for each item — square metres, running metres, numbers (Nos.), per flat, per unit, cubic metres, and so on

- Rate structure — are rates all-inclusive, or are there separate rates for material and labour? Are there escalation clauses tied to a price index?

- Payment milestones — some contracts pay purely on measured quantity; others release payment only on completion of defined milestones (e.g., “40% on structure completion”)

- Deductions — the exact percentages for TDS, retention money, and advance recovery, and the exact base amount each deduction is calculated on (gross amount, or gross plus GST this detail varies by contract and catches people out constantly)

I cannot stress this enough: a mistake at this stage becomes the wrong basis for the entire bill. If you misread the unit of measurement for one BOQ item, every quantity, every amount, and every downstream sheet built from it will be wrong and it is often only caught much later, when the client’s engineer cross-checks against the original BOQ.

Practical tip: Keep a one-page “Contract Summary” note (this is exactly what the Work Order Details sheet in the attached template is for) listing scope, units, rates basis, milestones, and deduction percentages. Refer back to this note every single time you prepare a new RA bill for that project, rather than re-reading the entire contract each month.

Step 2: Measurement Data Collection

Once you understand the contractual basis, the next task is collecting the actual quantities of work executed. This data comes from:

- Site engineer records — daily or weekly logs of work completed

- The MB (Measurement Book) — the physical or digital register where measurements are formally recorded and, ideally, countersigned by both contractor and client representatives at site

- Execution logs — progress photographs, daily activity reports, material consumption records that corroborate the quantities being claimed

There are generally two types of measurement, and it is worth knowing which one applies to your project because it changes how your Measurement Sheet should be structured:

- Item-based measurement — quantities are measured against individual BOQ items (for example, square metres of external painting, running metres of pipeline laid)

- Unit-based measurement — quantities are counted per discrete unit (for example, flats counted as 3BHK or 4BHK units, where a single “unit” bundles multiple BOQ items together)

In residential and commercial building projects, unit-based measurement is extremely common you will often see billing structured around “flats completed” rather than raw square metres, because it is easier for both sides to verify and track against the sale/possession schedule.

Practical tip: Whichever type applies, never record measurement data directly into your billing Excel file from memory or from a WhatsApp message. Always trace it back to a specific MB page number or execution log reference. This single habit is what makes your bill defensible during any later query.

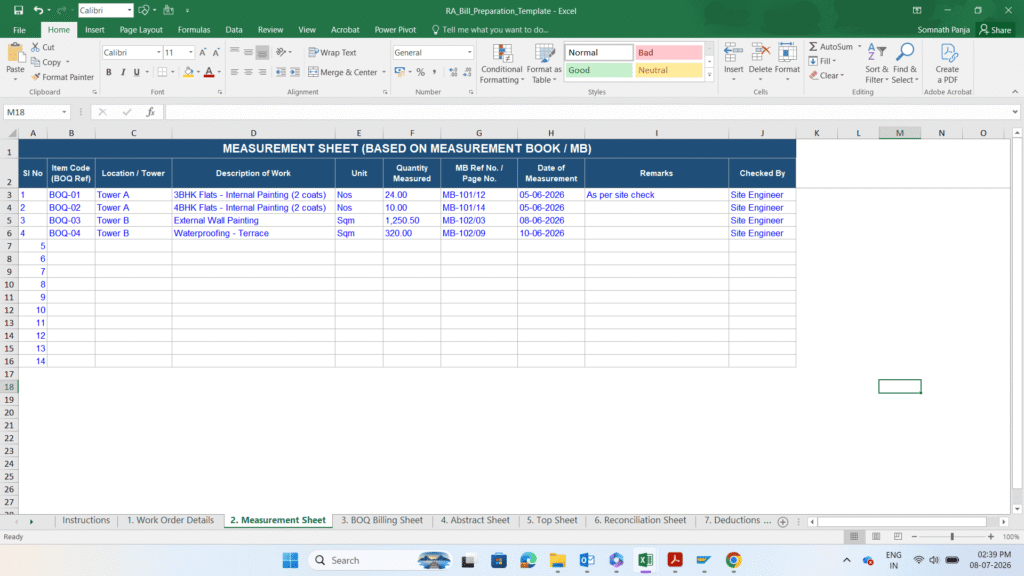

Step 3: Measurement Sheet Preparation

This is your foundation sheet in Excel — everything above it (BOQ Billing, Abstract, Top Sheet) is built from what you enter here. Structure it with, at minimum, these columns:

- Location / Tower (if the project has multiple buildings or zones)

- Description of the work

- Unit of measurement

- Quantity measured

- MB reference number and page/date

- Remarks

- Checked-by (name of the person who verified the measurement at site)

Best practices I follow on every project:

- Keep tower-wise or zone-wise sheets separate, or at least clearly filterable, if the project spans multiple buildings. Mixing everything into one undifferentiated list makes it very hard to reconcile later, especially if different towers are at different stages of completion.

- Use sequential, permanent numbering for each row (Sl No.) so that once a row is created, it is never renumbered in a later bill this protects your audit trail. If you need to add a new item mid-project, add it at the bottom with a new number rather than inserting rows and shifting the sequence.

- Never mix “measured” and “estimated” quantities in the same column without a clear remark. If a quantity is provisional pending final joint measurement, say so explicitly in the Remarks column.

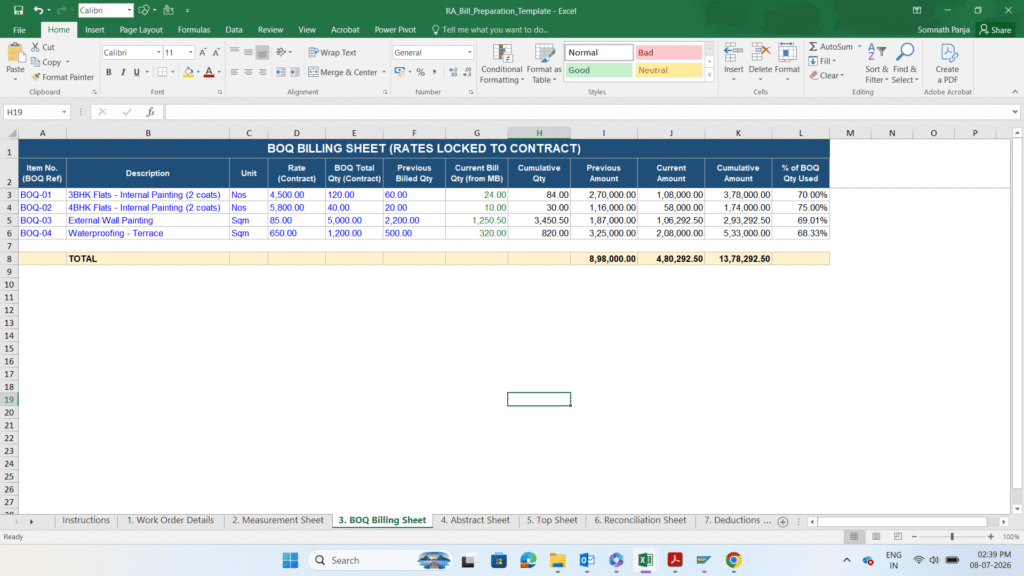

Step 4: BOQ Billing Sheet Preparation

This is where engineering quantity becomes money. The basic structure is:

| Item No. | Description | Unit | Rate | Qty | Amount |

|---|

And the core formula, deceptively simple but absolutely critical, is:

Amount = Quantity × Rate

The critical discipline at this step is around the Rate column:

- Rates must be copied exactly from the signed contract/BOQ — never estimated, never rounded, never adjusted for “what feels fair” this month.

- No manual overrides are allowed. If a rate genuinely needs to change (say, due to an approved variation or escalation clause), that change must come through a formal contract amendment first, and only then should the rate cell be updated with a clear note referencing the amendment.

- I recommend structuring your Excel sheet so the Rate column pulls from a locked reference table (or is at least visually locked/protected), so that nobody on the team can accidentally overwrite it while typing quickly.

In my attached template, the BOQ Billing Sheet is designed to automatically pull the “current quantity” figure from the Measurement Sheet using a lookup formula, rather than requiring you to retype it. This single link is what prevents the classic error of the Measurement Sheet saying one quantity and the BOQ Billing Sheet saying another, purely due to manual re-entry.

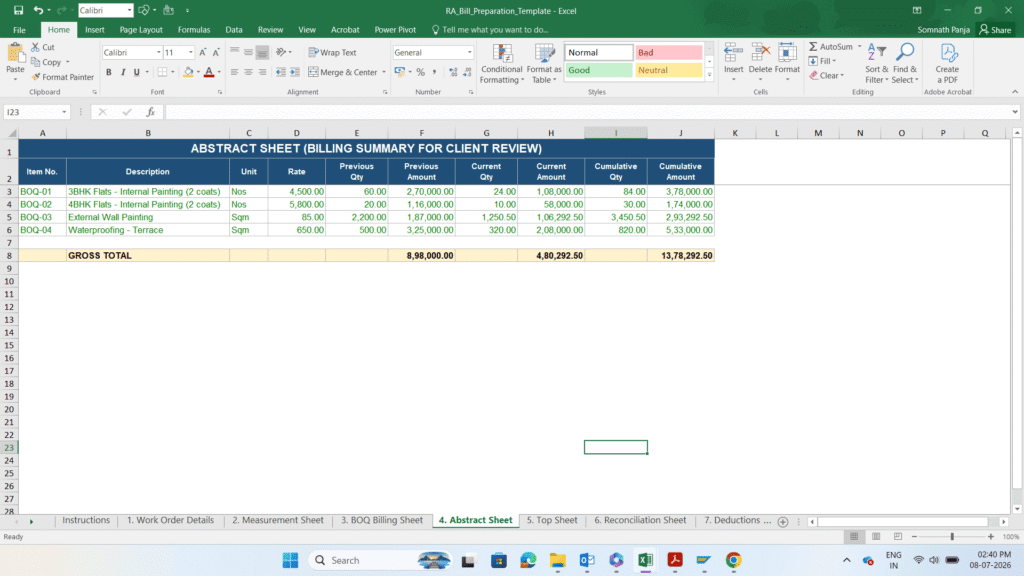

Step 5: Abstract Sheet Preparation

The Abstract is a summary sheet, and it deserves special attention because it is usually the very first thing the client’s billing engineer or project manager looks at. If your Abstract is clean, logical, and clearly laid out, it sets the tone for how the rest of the bill is reviewed.

The Abstract should show, for every BOQ item:

- Previously billed quantity (cumulative up to the last RA bill)

- Current billing quantity (this RA bill only)

- Cumulative quantity (previous + current)

- Corresponding amounts for each of the above

Think of the Abstract as the “executive summary” of your billing someone should be able to look at just this one sheet and understand exactly how much work has been billed to date, without needing to dig into the full Measurement Sheet.

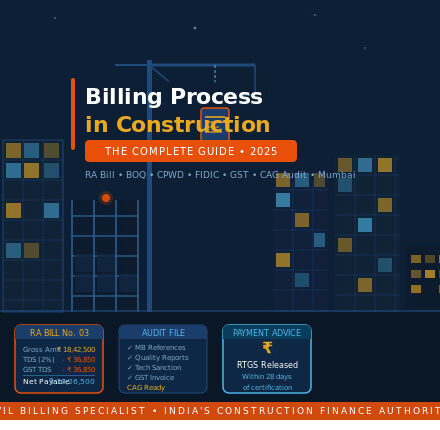

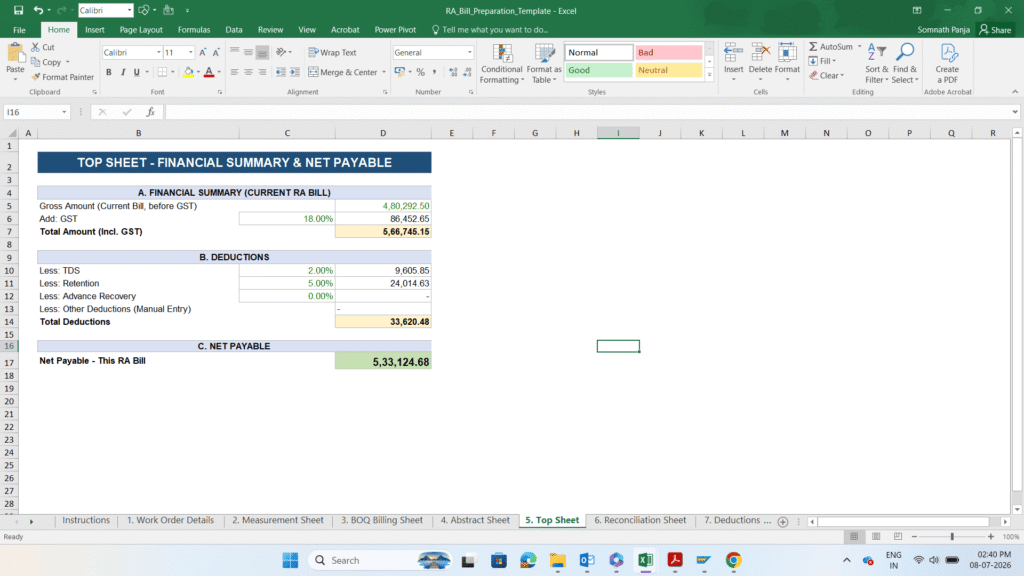

Step 6: Top Sheet Preparation

If the Abstract is the executive summary of quantities, the Top Sheet is the executive summary of money. This is arguably the single most scrutinised sheet in the entire bill, because it is what determines the actual payment amount. I break it into three clear sections:

A. Financial Summary

- Gross amount (from the Abstract’s current billing total)

- GST (calculated at the applicable rate on the gross amount)

- Total amount (gross plus GST)

B. Deductions

- TDS (Tax Deducted at Source), at the rate specified in the contract

- Retention money, held back as security until defect liability period completion or as per contract terms

- Advance recovery, if the contractor received a mobilisation advance that is being recovered proportionally against each RA bill

- Any other project-specific deductions (penalty for delay, material supplied by client and recovered, etc.)

C. Net Payable

- Total amount minus total deductions this is the actual figure the client is expected to pay against this RA bill

A word of caution on deduction bases: different contracts calculate TDS, retention, and advance recovery on different bases — some on the gross (pre-GST) amount, some on the total (post-GST) amount. This is exactly the kind of clause-level detail from Step 1 that must be locked in correctly, because getting the base wrong produces a Net Payable figure that is subtly, and sometimes significantly, incorrect.

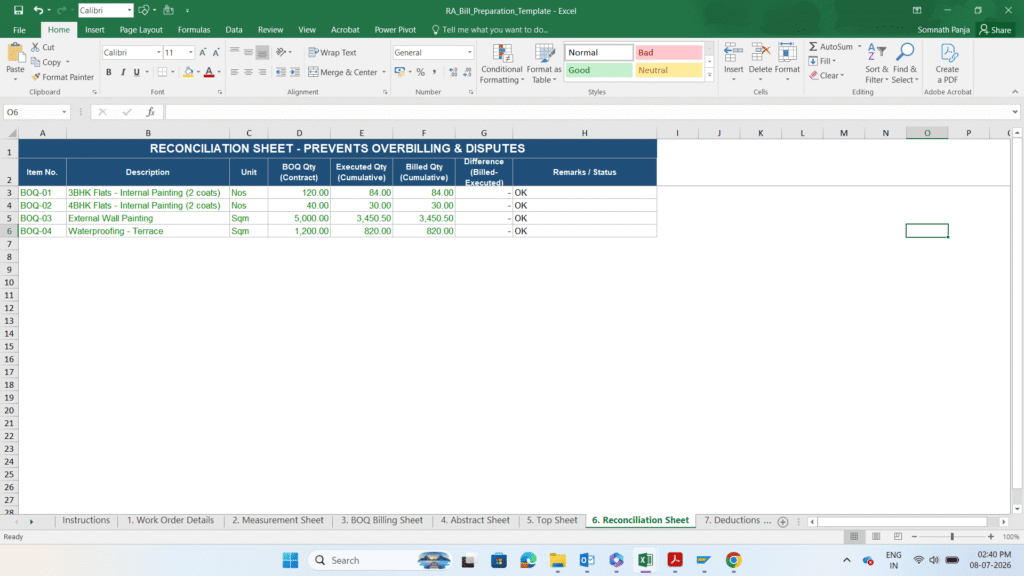

Step 7: Reconciliation Sheet

This sheet exists purely to protect you from disputes, and I consider it one of the most underused tools in construction billing. Structure it as:

| Item | BOQ Qty (Contract) | Executed Qty | Billed Qty | Difference |

|---|

The purpose is simple but powerful:

- Ensure no overbilling — the cumulative billed quantity for any item should never exceed the executed (measured) quantity, and should certainly never exceed the total BOQ quantity in the contract without a formal variation order.

- Justify all quantities — if there is any difference between executed and billed quantity (for example, work executed but intentionally held back from billing this cycle for internal reasons), that difference should be visible and explainable, not hidden inside a larger cumulative number.

I have made it a personal rule to never submit a bill where the Reconciliation Sheet shows an unexplained mismatch. It takes five extra minutes to check, and it can save weeks of back-and-forth with the client later.

Step 8: Invoice Matching

Once your Abstract and Top Sheet are finalised, the contractor’s tax invoice must be prepared to match them exactly:

- The invoice’s taxable value must match the Abstract’s gross current billing amount

- The GST amount and rate on the invoice must match the Top Sheet’s GST calculation

- The invoice number, date, and period should be consistent with the RA bill number and billing period stated elsewhere in the package

The most common mistake at this step, and one I have personally seen delay payments for weeks, is a simple mismatch between the invoice total and the Abstract total sometimes due to a rounding difference, sometimes because someone updated the Abstract after the invoice was already generated and forgot to regenerate the invoice. Whenever the bill changes, even by a small amount, the invoice must be checked again before submission. A payment can genuinely go on hold purely because of this mismatch, regardless of how correct every other part of the bill is.

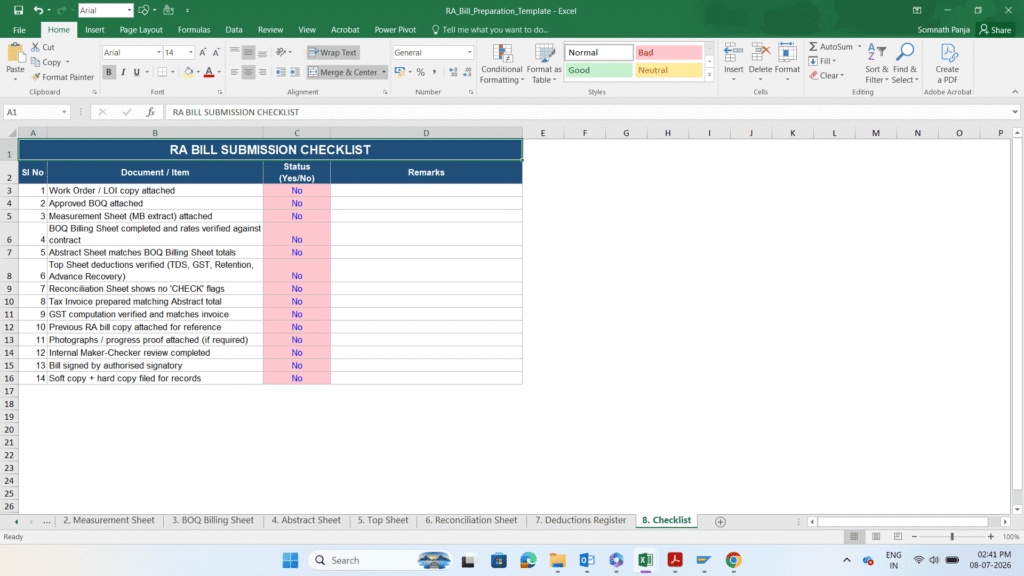

Step 9: Checklist Creation

The final step before submission is running through a checklist that confirms:

- No document from the five layers described in Part 2 is missing

- Every sheet’s totals tie out against every other sheet (Measurement → BOQ Billing → Abstract → Top Sheet → Invoice)

- Internal maker-checker review has been completed and signed off

A good checklist does two things: it prevents missing documents (which cause rejection), and it speeds up approval on the client’s side, because their reviewer does not have to chase you for anything.

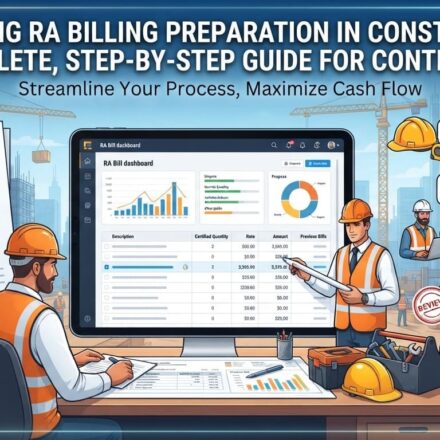

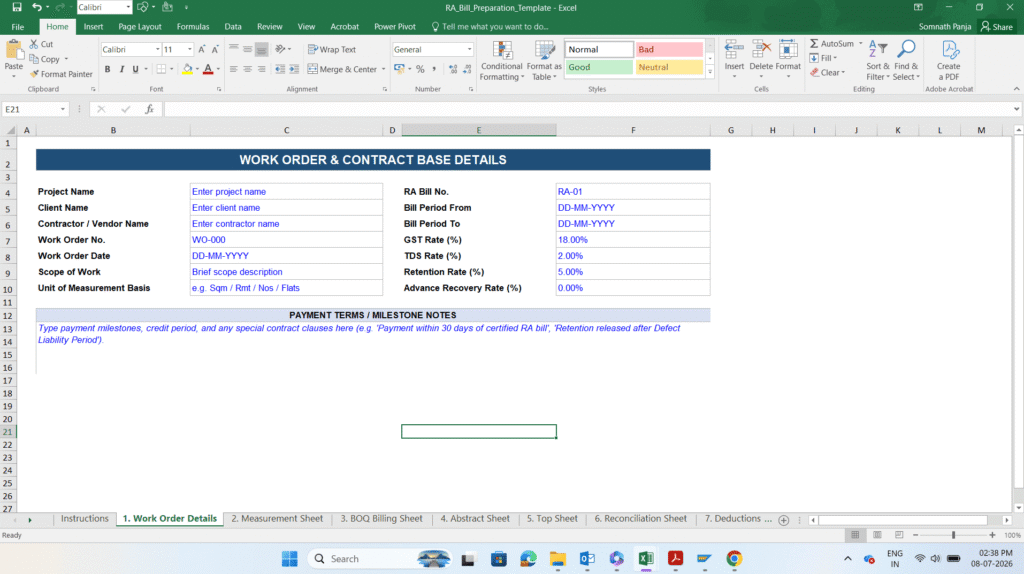

How the Excel Template Is Structured

I have built the attached Excel workbook RA_Bill_Preparation_Template.xlsx so that it mirrors the process above exactly, sheet by sheet, and can be reused by any contractor on any project, not just the specific example I’ve built into it. Here is what each tab does and how they connect to each other.

Sheet 0 — Instructions: A one-page guide inside the workbook itself, explaining how to use each sheet, the colour-coding convention used throughout (blue = input you type, black = formula, green = a link pulled from another sheet), and a set of “important notes” that flag the most common pitfalls.

Sheet 1 — Work Order Details: This is where you enter the project name, client name, contractor name, work order number and date, scope, RA bill number, billing period, and critically the GST, TDS, retention, and advance recovery percentages. Every other sheet in the workbook pulls its rates and percentages from this one sheet, so updating a rate here automatically flows through the entire bill.

Sheet 2 — Measurement Sheet: A structured log for recording quantities executed at site, tagged with an Item Code that links back to the BOQ, along with location/tower, MB reference, date, and the name of the person who checked the measurement.

Sheet 3 — BOQ Billing Sheet: Lists every contract item with its locked rate and total BOQ quantity. The “current bill quantity” column automatically sums the relevant rows from the Measurement Sheet using a lookup formula, so you never have to manually re-type a quantity that already exists elsewhere. It then calculates previous, current, and cumulative amounts automatically, plus a percentage showing how much of the total BOQ quantity has been consumed a useful early warning if an item is approaching its contractual limit.

Sheet 4 — Abstract Sheet: Automatically pulls its figures from the BOQ Billing Sheet, presenting the same information in the clean summary format a client reviewer expects to see first.

Sheet 5 — Top Sheet: Pulls the current gross billing amount from the Abstract, applies GST from the Work Order Details sheet, then calculates TDS, retention, and advance recovery deductions, arriving at a final Net Payable figure for this RA bill.

Sheet 6 — Reconciliation Sheet: Compares BOQ quantity, executed quantity, and billed quantity side by side, and automatically flags any row where billed quantity exceeds executed quantity, or executed quantity exceeds the contractual BOQ quantity highlighting it in red so it cannot be missed before submission.

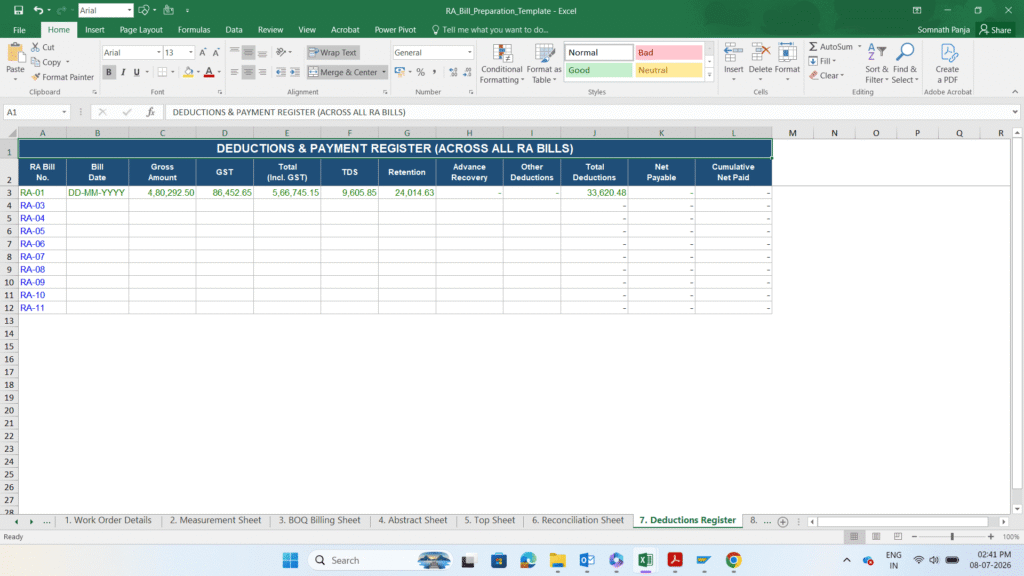

Sheet 7 — Deductions Register: A running ledger across every RA bill raised on the project so far, tracking gross amount, GST, all deductions, net payable, and a cumulative net-paid total this becomes your project’s payment history at a glance, useful for cash flow planning and for quickly answering “how much has the client paid us to date?”

Sheet 8 — Checklist: A tick-list of every document and verification step that should be completed before the bill leaves your desk, with colour-coded status (red for “No,” green for “Yes”) so an incomplete bill is visually obvious at a glance.

Because every downstream sheet is linked with formulas rather than retyped values, updating the Measurement Sheet each month automatically flows through to the BOQ Billing Sheet, Abstract, Top Sheet, and Deductions Register this is precisely the kind of internal consistency that prevents the invoice-mismatch and overbilling problems described earlier.

A short worked example, using the sample data already loaded into the template: across four illustrative BOQ items (internal painting for 3BHK and 4BHK flats, external wall painting, and terrace waterproofing), the current bill quantities produce a gross current billing amount that, once GST is added and TDS, retention, and advance recovery are deducted, arrives at a clear net payable figure on the Top Sheet — you can see the entire chain, from a single measurement entry to the final payable amount, simply by opening the workbook and following the linked cells from one sheet to the next.

IS CODE reference

Indian Standard (IS) codes are essential references for civil engineering in India. Accessing these specific standards is vital for verifying material quality, structural loads, and design regulations.

Below is the list of key IS codes grouped by category, with links to where you can find and review the standards and their technical details:

Key IS Codes for Civil Engineering

- Concrete & Materials: Key standards include IS 456:2000 (Concrete Design), IS 383:2016 (Aggregates), IS 10262:2019 (Mix Design), and IS 516:2018 (Concrete Testing).

- Structural & Loads: Core codes are IS 800:2007 (Steel), IS 875:1987 (Loads), and IS 1893:2016 (Earthquake).

- Geotechnical: Primary standards include IS 2720 (Soil Testing), IS 6403:1981 (Foundation), and IS 2911 (Piling).

- Materials & Estimation: Essential codes are IS 1077:1992 (Bricks), IS 269:2015 (Cement), IS 1200 (Measurement), and IS 13920:2016 (Seismic Detailing).

Why a Structured Billing System Matters

It’s worth stepping back from the mechanics for a moment and talking about why all of this effort is worthwhile.

5.1 Financial Accuracy

A structured system with locked rates, cross-checked quantities, and a reconciliation sheet is the single best defence against revenue leakage — the slow, often invisible loss of money through undercounted quantities, missed items, or rates applied incorrectly. Over the life of a large project, even small percentage leaks compound into significant amounts.

5.2 Faster Payments

Clients do not delay payment out of malice — they delay payment when a bill requires clarification, correction, or chasing for missing documents. A complete, well-documented bill, submitted with every supporting document already attached, removes the client’s excuse to hold payment. In my experience, the single biggest lever for faster payment cycles is not negotiating better contract terms — it is simply submitting a bill that requires zero back-and-forth.

5.3 Audit Readiness

Whether it is an internal audit by the contractor’s own finance team, a statutory audit, or a client’s post-completion reconciliation, the auditor’s first question is almost always: “Can you show me the trail from measurement to payment?” A structured system where every quantity traces back to an MB reference, every rate traces back to the Work Order, and every bill is version-controlled answers that question instantly.

5.4 Client Trust

Transparent billing where the client can see exactly how a number was arrived at, rather than being presented with an opaque lump sum builds trust over the life of a relationship. Contractors who consistently submit clean, well-organised bills often find that subsequent bills are certified faster, simply because the client’s team has learned to trust the source.

5.5 Team Efficiency

When every billing engineer on a team uses the same template and the same process, work becomes interchangeable. Someone can step in for a colleague who is on leave, a new team member can be onboarded quickly, and the client-facing quality of bills stops depending on which individual happened to prepare it that month.

Major Risks in RA Billing — and Why They Happen

Understanding why errors happen is more useful than just knowing they exist. Here are the six risks I see most often, along with their root causes and consequences.

Risk 1: Quantity Errors

Cause: Wrong measurement at site, or missing data that gets estimated rather than actually measured. Impact: Underbilling (the contractor loses money that can rarely be recovered later) or overbilling (which creates a liability that must eventually be adjusted, often awkwardly, in a future bill).

Risk 2: Rate Errors

Cause: An incorrect rate pulled from an outdated BOQ version, or a manual override applied without proper authorisation. Impact: Direct financial loss to the contractor if the rate is too low, or a dispute and potential rejection if the rate is too high relative to the signed contract.

Risk 3: Lack of Supporting Documents

Cause: A missing MB reference, or no backup sheet justifying a claimed quantity. Impact: Straightforward bill rejection clients are increasingly strict about not certifying bills that cannot be immediately backed up with source documents.

Risk 4: Invoice Mismatch

Cause: Different values appearing on the tax invoice versus the Abstract Sheet, usually because one was updated after the other. Impact: Payment delay, because most client finance teams will not process a payment until the invoice and supporting bill numbers agree.

Risk 5: Ignoring Contract Clauses

Cause: A deduction (TDS, retention, escalation adjustment) that should have been applied per the contract, but wasn’t often simply because the person preparing the bill did not go back to Step 1 and re-read the contract terms carefully. Impact: A financial dispute later, when the client’s finance team catches the missed deduction and either claws it back from a future payment or raises a formal query.

Risk 6: Overbilling Risk

Cause: No reconciliation process in place, so cumulative billed quantities silently creep past executed or even contractual quantities without anyone noticing. Impact: This is the most serious of the six it is precisely the kind of issue that turns into a serious audit objection, because it can look, even unintentionally, like a deliberate overstatement of work done.

Risk Mitigation Strategies

For every risk above, there is a corresponding, practical control. Here is what I actually put in place on my projects.

1. A Standard Excel Template

The single biggest structural fix is simply not reinventing the wheel every month. Using one consistent template (like the one attached to this guide) across every RA bill on a project avoids structural errors, missing sheets, and inconsistent formatting that make bills harder to review.

2. A Maker-Checker System

One person prepares the bill. A different person ideally someone senior enough to catch conceptual errors, not just typos checks it before it is sent to the client. This single control catches an enormous share of errors before they ever leave the office, because a fresh set of eyes reviewing the numbers against the contract will notice things the preparer, deep in the detail, may miss.

3. Quantity Cross-Verification

Before finalising a bill, cross-check quantities across three sources: the MB, the BOQ Billing Sheet, and the Abstract. If all three agree, you have strong confidence in the numbers. If they don’t, you have caught a problem before the client did.

4. Locked Rate Cells

Wherever possible, protect the Rate column in your BOQ Billing Sheet so it cannot be accidentally edited during data entry. Even a well-intentioned team member correcting what looks like a typo can inadvertently introduce a serious rate error if the cell isn’t protected.

5. A Mandatory Checklist

No bill leaves your desk without every item on the checklist marked complete. This is the final gate before submission, and it should be treated as non-negotiable, not as an optional nicety.

6. Version Control

Every RA bill should be saved as its own distinct, clearly named file (RA-01, RA-02, RA-03, and so on) rather than continuously overwriting the same file. This avoids duplicate submissions, protects your history, and makes it trivial to answer “what did we submit last month?” months or years later.

Advanced Best Practices for Billing Managers

Once the basic process above is running smoothly, there are a few additional practices that separate a good billing system from a genuinely excellent one.

1. Dashboard Reporting

At the project or portfolio level, maintain a simple dashboard tracking billed-versus-executed quantities and pending certifications across all active RA bills. This gives management an early warning if a particular bill is stuck, or if billed quantities are consistently lagging behind actual site progress (a sign that billing is falling behind, which itself creates cash flow strain).

2. Digitalisation

Where feasible, move from isolated desktop files to a shared platform a shared Excel file on Teams or SharePoint, or a dedicated billing software with auto-calculation and access control. This reduces the risk of multiple people editing conflicting local copies of the same bill.

3. An Internal Audit Sheet

Before a bill goes to the client, run it past an internal audit checklist that is stricter than the client-facing checklist checking not just for completeness, but for arithmetic accuracy, clause compliance, and consistency with prior bills. Think of this as a dress rehearsal for the scrutiny the bill will face externally.

4. Variation Tracking

Maintain a separate, dedicated log for extra items and deviations from the original BOQ. Variations are one of the most common sources of billing disputes precisely because they sit outside the “clean” original contract structure if they are not tracked separately and clearly justified, they tend to become contentious later.

Common Mistakes to Avoid — A Quick-Reference List

Before I close, here is a condensed list of the mistakes I have seen cause the most trouble, worth pinning up next to your desk:

- Copy-pasting figures from a previous bill without re-checking that they still apply

- Manual calculation errors that a simple formula-based sheet would have prevented entirely

- Missing GST reconciliation between the invoice and the Top Sheet

- Submitting quantities with no clear MB or measurement justification

- Sending an incomplete file missing even one annexure or supporting document

If you take nothing else from this entire guide, take this: almost every one of these mistakes is prevented simply by following the nine-step process in order, using a single consistent template, and never skipping the checklist at the end.

A Quick-Reference Glossary

Since this guide uses a lot of terminology that is standard on site but can be confusing to someone new to billing, here is a plain-language glossary I keep handy for training new team members:

- RA Bill (Running Account Bill): A periodic bill raised by the contractor for work executed and measured up to a given date, as against a single final bill at project completion.

- MB (Measurement Book): The register physical or digital where site measurements are formally recorded, ideally jointly signed by contractor and client representatives.

- BOQ (Bill of Quantities): The contractually agreed list of items, units, and rates against which all billing is done.

- Abstract: A summary sheet showing previous, current, and cumulative quantities and amounts for every BOQ item.

- Top Sheet: The final financial summary sheet gross amount, GST, deductions, and net payable.

- TDS (Tax Deducted at Source): A statutory deduction the client withholds from the contractor’s payment and deposits with the tax authorities on the contractor’s behalf.

- Retention Money: A percentage of each bill withheld by the client as security, usually released after the defect liability period.

- Advance Recovery: The proportional deduction of a mobilisation or other advance already paid to the contractor, recovered against each RA bill until fully adjusted.

- Reconciliation: The process of comparing BOQ quantity, executed quantity, and billed quantity to ensure no overbilling has occurred.

- Maker-Checker: A basic internal control where one person prepares a document and a different person independently reviews it before it is finalised.

A Short Case Study — Walking Through One RA Bill

To make all of this concrete, let me walk through a simplified example, close to what you’ll find already loaded into the attached Excel template.

Imagine a residential tower project with four billable items: internal painting for 3BHK flats, internal painting for 4BHK flats, external wall painting, and terrace waterproofing. At the start of the month, the site engineer records fresh measurements in the Measurement Sheet so many flats painted, so many square metres of external wall covered, so much waterproofing area completed each entry tagged with its MB reference and the date it was checked.

Because the BOQ Billing Sheet is linked to the Measurement Sheet, these quantities flow through automatically the moment they’re entered there’s no need to manually retype anything. The sheet applies the locked contract rate for each item, calculates the amount for work billed previously, the amount for this month’s current billing, and the cumulative amount to date. It also quietly checks what percentage of the total contracted quantity has now been consumed for each item useful information if an item is nearing its contractual limit and might need a variation order soon.

The Abstract Sheet then pulls this same data into the clean, summarised format the client’s team will actually review first. From there, the Top Sheet takes the current gross billing figure, adds GST at the applicable rate, and works out TDS, retention, and advance recovery deductions arriving at one final number: the net amount payable for this particular RA bill.

Before the bill goes anywhere, the Reconciliation Sheet does one last job: it checks that the billed quantity for every item is not exceeding either the quantity actually executed at site or the total quantity allowed under the contract. If everything checks out, every row simply reads “OK.” If something doesn’t add up, the sheet flags it in red immediately, well before the client ever sees the bill.

Only once the Checklist confirms every supporting document is attached Work Order, BOQ, measurement backup, invoice matching the Abstract does the bill actually go out. This is the same sequence, every single month, for every RA bill on the project. Nothing about it depends on who happens to be preparing it that week.

Editor’s Pick

Read more: Standardized Excavation Measurement Benchmark – IS Code Explained

Read more: Standardized Excavation Measurement Benchmark – IS Code ExplainedStandardized Excavation Measurement Benchmark – IS Code Explained

on

- Read more: Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

on

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

on

Read more: Basic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red Flags

Read more: Basic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red FlagsBasic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red Flags

on

Frequently Asked Questions

Q: What if the client disputes a quantity after the bill is submitted? This is exactly why the Reconciliation Sheet and MB references matter so much. If every quantity in your bill traces back to a specific, dated measurement entry ideally one that was jointly checked at site a dispute becomes a quick conversation about one specific line item, not a re-audit of the entire bill.

Q: Should retention money be shown as a deduction, or tracked separately? Both. It should be deducted from the current bill’s net payable (so the contractor isn’t overpaid), and it should also be tracked in a running register (like the Deductions Register in the attached template) so that the cumulative retention balance the amount eventually due back to the contractor is always visible.

Q: How do I handle a rate change mid-project? Never edit the original rate cell directly. Instead, treat a rate change as a formal contract amendment: get it documented and approved first, then update the rate in your billing sheet with a clear note referencing the amendment number and date, so the change is traceable rather than looking like an unexplained edit.

Q: What’s the difference between the Abstract and the Top Sheet? The Abstract is about quantities and item-wise amounts it answers “how much of each item has been billed.” The Top Sheet is about the final payable figure it answers “how much money does the client actually owe after tax and deductions.” Both matter, but they answer different questions for different audiences.

Q: Can this same template be used for subcontractor billing, not just client billing? Yes, the underlying logic (measurement → BOQ billing → abstract → deductions → net payable) is identical whether the bill is going from contractor to client, or from subcontractor to main contractor. Only the specific deduction percentages and contract terms in the Work Order Details sheet need to change.

Conclusion

A professional RA billing system is really a combination of three disciplines working together: engineering accuracy in measurement, financial discipline in calculation, and documentation control in how everything is recorded and filed. None of the three, on its own, is enough, a perfectly measured quantity billed at the wrong rate is just as much of a problem as a perfectly calculated amount with no measurement backup behind it.

What I have tried to lay out in this guide and what the attached Excel template is built to support is a repeatable process: understand the contract, collect and record measurements properly, calculate billing on locked rates, summarise it cleanly for the client, reconcile it against both the contract and the site reality, match it to the invoice, and check it one final time before it leaves your hands.

Used consistently, this kind of system delivers exactly the outcomes every contractor and every client project team actually wants: faster approvals, fewer disputes, and a billing trail strong enough to survive any audit.

I built the attached workbook so that any contractor, on any project, regardless of size, can pick it up and start using this exact process on their very next RA bill simply fill in your Work Order Details, start logging measurements, and let the linked formulas carry the rest of the work through to a clean, defensible Net Payable figure.

Follow the below links for more blogs………..

RA Bill Checking: Complete Audit accomplished Framework for Civil Engineers