")

STEEL RECONCILIATION | The Complete Guide to Preparing a Contractor | Material Reconciliation Statement (MRS)

Introduction: What Is Steel Reconciliation and Why It Matters

Steel reconciliation is the process of matching the quantity of reinforcement steel received, issued, and consumed at a construction site against the quantity theoretically required as per the structural drawings. It is, without question, the single most argued-over exercise in any construction contract, because steel is expensive, it is measured in tonnes, and even a half-percent error in a steel reconciliation statement can swing lakhs of rupees at final billing.

Yet, in my experience, very few engineers — even senior ones — understand the complete chain of logic behind a proper steel reconciliation. Most treat it as a simple subtraction: “issued minus used equals wastage.” In reality, a defensible material reconciliation statement (MRS) for steel must account for rolling margin, theoretical quantity from the Bar Bending Schedule (BBS), extra steel not meant for billing, unbilled quantity, reusable cut pieces, and two entirely different categories of wastage.

This guide walks through the full steel reconciliation process, step by step, exactly the way I have built and audited these statements over the years — simple in language, but with every formula that is actually used in practice.

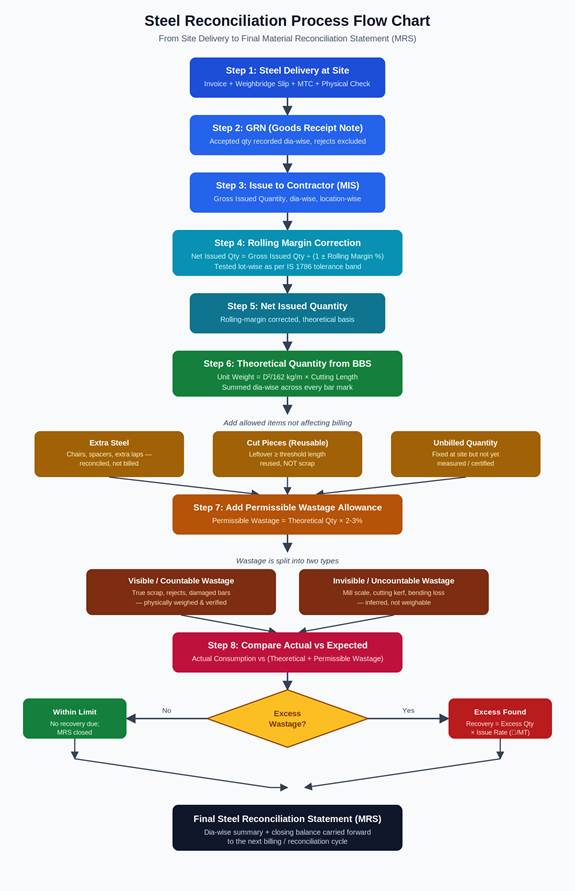

Steel Reconciliation Process Flow Chart

Before we go stage by stage, it helps to see the entire steel reconciliation process at a glance. The flow chart below maps every stage discussed in this guide, from the first truck at the site gate to the final, dia-wise Material Reconciliation Statement.

Flow chart: The complete steel reconciliation process, from delivery at site to the final Material Reconciliation Statement (MRS).

Keep this flow chart in mind as you read — each stage corresponds to a section below.

Delivery of Steel at Site — The Starting Point of Steel Reconciliation

1.1 What Should Accompany Every Delivery

Every steel reconciliation exercise starts at the site gate. Steel must never be accepted on trust — every truckload of TMT reinforcement bars must be accompanied by:

- Tax Invoice / Commercial Invoice — dia-wise quantity in MT and rate

- Weighbridge Slip — gross weight, tare weight, net weight

- Mill Test Certificate (MTC) — chemical/physical properties, heat number, batch number

- Delivery Challan (DC) — dia-wise, bundle-wise breakup

- E-way Bill — statutory movement document

The first discipline of accurate steel reconciliation begins here: never accept a “consolidated” weight without a dia-wise breakup. If 12mm, 16mm, and 25mm bars arrive together under one lump weight figure, you lose the ability to reconcile dia-wise later. Always insist on bundle-wise, dia-wise weight.

1.2 Physical Verification at Site

- Re-weighment at site weighbridge — a tolerance of ±0.5% against the supplier’s weighbridge is generally acceptable; anything beyond must be investigated.

- Physical bundle count — bundle count × bars per bundle × standard length × unit weight per meter should broadly match the invoiced weight.

- Visual inspection — rust condition, bends, dia consistency within a bundle.

- Sample testing — as per IS 1786:2008, tensile strength, yield strength, elongation, and bend/rebend test from each heat number.

Almost every error I have ever traced in a final steel reconciliation statement originated at this delivery stage — usually poor dia-wise segregation, or “received quantity” being taken from the invoice instead of the actual weighbridge/physical verification. Get this stage disciplined and 80% of reconciliation trouble disappears before it starts.

Goods Receipt Note (GRN) — The First Formal Record in Steel Reconciliation

2.1 What a GRN Represents

The GRN is the internal document confirming: “This much material has been received, verified, and accepted into site stock.” It is the bridge between the supplier’s invoice and the contractor’s issue register, and it is the true foundation of the entire steel reconciliation process — nothing should be issued to a contractor without first passing through a GRN.

2.2 Contents of a Proper GRN

| Field | Why It Matters for Steel Reconciliation |

| GRN Number & Date | Traceability |

| Supplier Invoice Number | Cross-reference to purchase |

| Dia-wise Quantity (MT) | Foundation for dia-wise reconciliation |

| Heat/Batch Number | Traceability to MTC and rolling margin test |

| Accepted / Rejected Quantity | Only accepted qty enters stock |

| Weighbridge Slip Reference | Audit trail |

| Running Cumulative Receipt | Directly feeds the final MRS |

2.3 GRN Quantity vs Invoice Quantity

Always record the GRN quantity as actual accepted weight, not invoiced weight. If the invoice shows 10.000 MT but 0.150 MT is rejected on a bend-test failure, the GRN reflects 9.850 MT accepted. This cumulative accepted figure across all GRNs becomes the single most important number in steel reconciliation — the Total Quantity Received at Site:

Total Received (GRN Cumulative) = Σ (Accepted Weight per GRN)

Issue of Steel to Contractor

3.1 The Material Issue Slip (MIS)

Once steel is in store, it is issued to the contractor against a specific work front — a slab, a column grid, a footing — through a Material Issue Slip (MIS) recording date, dia, quantity, location, and the contractor’s signed acknowledgment.

3.2 Gross Issued Quantity

Gross Issued Quantity (GIQ) = Σ (Quantity issued per MIS, dia-wise)

This is the quantity physically handed over — but in steel reconciliation, Gross Issued Quantity is never directly compared against the theoretical requirement. It must first pass through the rolling margin correction, which is the next, and most misunderstood, part of the process.

Rolling Margin — The Most Misunderstood Concept in Steel Reconciliation

4.1 What Is Rolling Margin?

TMT bars are manufactured by hot-rolling steel billets, and this process cannot produce a bar of exactly the theoretical unit weight every time. IS 1786:2008 permits a manufacturing tolerance on the theoretical weight per meter, called Rolling Margin:

| Nominal Diameter | Permissible Tolerance on Weight |

| Up to and including 10mm | ±7% |

| Above 10mm up to 16mm | ±5% |

| Above 16mm | ±3% |

(Always cross-check against the current IS 1786 edition and the specific mill’s declared tolerance sheet, since some contracts negotiate tighter bands.)

4.2 Why Rolling Margin Matters in Steel Reconciliation

Since steel is purchased and issued by weight but consumed by length (a beam needs a bar of a certain length, not a certain weight), this weight-versus-length mismatch must be reconciled — and that is exactly what rolling margin correction does in a proper steel reconciliation.

4.3 How to Calculate Rolling Margin

Method A — Actual Test-Based Rolling Margin (Preferred):

- Cut a sample of known length (e.g., 3m) from each lot/heat.

- Weigh it accurately.

- Calculate actual unit weight.

Actual Unit Weight (kg/m) = Weight of Sample (kg) ÷ Length of Sample (m)

Compare against theoretical unit weight (see Part 5):

Rolling Margin (%) = [(Actual Unit Weight − Theoretical Unit Weight) ÷ Theoretical Unit Weight] × 100

A positive rolling margin (heavier-than-theoretical bars) benefits the owner — less weight is consumed for the same length. A negative rolling margin (lighter bars) means more weight is consumed for the same length.

Method B — Bundle-Based Rolling Margin (Faster, Common on Site):

Rolling Margin (%) = [(Actual Bundle Weight ÷ Total Bundle Length) − Theoretical Unit Weight] ÷ Theoretical Unit Weight × 100

4.4 How Rolling Margin Changes the Net Issued Quantity

This is the crux of accurate steel reconciliation. The Gross Issued Quantity (a weight figure) must be converted to an equivalent theoretical weight before it can be compared to the BBS-based theoretical requirement:

Net Issued Quantity = Gross Issued Quantity ÷ (1 + Rolling Margin % / 100)

Worked Example (Positive Rolling Margin):

Gross Issued Quantity (16mm) = 103.00 MT, Rolling Margin = +3%

Net Issued Quantity = 103.00 ÷ 1.03 = 100.00 MT

Although 103 MT was physically issued, the equivalent theoretical quantity actually needed to cover the required length is only 100 MT — the extra 3 MT is a legitimate rolling margin benefit, not a discrepancy.

Worked Example (Negative Rolling Margin):

Gross Issued Quantity = 103.00 MT, Rolling Margin = -3%

Net Issued Quantity = 103.00 ÷ 0.97 = 106.19 MT

Here, Net Issued Quantity is higher than gross issued — the lighter bars mean more weight was genuinely needed. This is why rolling margin must always be captured lot-wise and dia-wise; using a flat average across all diameters is a common, costly shortcut in steel reconciliation that leads directly to disputes.

Editor’s Pick

Read more: Standardized Excavation Measurement Benchmark – IS Code Explained

Read more: Standardized Excavation Measurement Benchmark – IS Code ExplainedStandardized Excavation Measurement Benchmark – IS Code Explained

on

- Read more: Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

on

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

on

Read more: Basic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red Flags

Read more: Basic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red FlagsBasic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red Flags

on

Net Issued Quantity vs Theoretical Quantity — The Core Comparison in Steel Reconciliation

5.1 What Is a BBS?

The Bar Bending Schedule (BBS) is the structural detailing document listing, per element, the bar mark, diameter, shape, cutting length, and number of bars required.

5.2 The Theoretical Unit Weight Formula

Every steel reconciliation converts length into weight using the standard IS 1786 formula:

W = D² ÷ 162 (kg/m)

Where D is nominal diameter in mm.

| Dia (mm) | Formula (D²/162) | Unit Weight (kg/m) |

| 8 | 64/162 | 0.395 |

| 10 | 100/162 | 0.617 |

| 12 | 144/162 | 0.888 |

| 16 | 256/162 | 1.580 |

| 20 | 400/162 | 2.469 |

| 25 | 625/162 | 3.858 |

| 32 | 1024/162 | 6.321 |

5.3 Calculating Theoretical Quantity from BBS

Total Length of a Bar Mark (m) = Cutting Length per bar × Number of bars

Theoretical Weight of a Bar Mark (kg) = Total Length × (D² ÷ 162)

Total Theoretical Quantity (MT) = Σ [Length × (D² ÷ 162)] ÷ 1000, summed across all bar marks

This is the absolute benchmark against which the rest of the steel reconciliation — Net Issued Quantity, wastage, and excess consumption — is measured.

5.4 Dia-wise Reconciliation Is Non-Negotiable

Every stage of steel reconciliation — Net Issued Quantity, Theoretical Quantity, and wastage — must be done dia-wise, never as a lump total. A contractor over-consuming 8mm while saving on 25mm can hide a real problem behind a deceptively balanced grand total. Reconcile dia by dia, and sum only at the final summary stage.

Extra Steel Considered in Reconciliation but NOT in Billing

Some items are accepted in steel reconciliation (they genuinely explain where the steel went) but are not billed to the client, because they fall outside the measured/certified BOQ item:

- Chairs and Spacers — fabricated from small-dia cut bars to maintain cover; consumed on site, reconciled, but generally not billed separately.

- Additional Laps/Splices Beyond BBS — extra laps introduced due to site handling constraints; a legitimate reconciliation item, not a billable one.

- Temporary Works Steel — dowels, bracing, and templates used during construction sequencing, later removed or scrapped.

- Rework/Replacement Steel — steel replacing damaged reinforcement; must be reconciled once, avoiding double-counting.

Principle: Reconciliation is a physical/quantity exercise (where did the steel go?); billing is a commercial/contractual exercise (what can be claimed for payment?). Keep the two conceptually separate, even though both draw on the same BBS and issue data.

Unbilled Quantity in Steel Reconciliation

Unbilled Quantity is reinforcement steel that has been issued and physically fixed at site, but not yet measured and certified for billing as of the reconciliation cut-off date — usually a timing mismatch between the billing cycle and the reconciliation cycle.

Quantity Reconciled = Billed Theoretical Quantity + Unbilled (Fixed but not yet Measured) Quantity

Without separating this out, a steel reconciliation statement will show a false mismatch that looks like excess wastage, when it is really just a timing difference. Unbilled quantity is a rolling figure — it moves into “billed” in the next cycle once measured.

Cut Pieces — Not Scrap, A Reusable Asset

8.1 The Core Concept

When a 12m standard bar is cut to the length required by the BBS, a leftover remainder is common. Example: cutting two 4.2m pieces from a 12m bar leaves 3.6m (12 − 4.2 − 4.2 = 3.6m). This 3.6m piece is not scrap — it is a reusable length for a shorter bar mark elsewhere (a stirrup, a dowel, a shorter lap).

8.2 Why This Distinction Matters

Reusable Cut Piece = Leftover length ≥ Minimum Reusable Threshold (typically 1.0m–1.5m, site-specific)

True Scrap = Leftover length < Minimum Reusable Threshold

Clubbing cut pieces with scrap artificially inflates the wastage percentage in steel reconciliation, unfairly penalizing the contractor. A well-run site maintains a Cut Piece Register, dia-wise, and reuses these lengths before cutting fresh standard bars — this is one of the few places in steel reconciliation where good site discipline shows up directly in the numbers.

Wastage in Steel Reconciliation — Visible and Invisible

9.1 Visible (Countable) Wastage

Physically collectible and weighable:

- True scrap pieces below the reusable threshold

- Rusted/corroded, rejected bars

- Bent/damaged bars during handling

- Cutting/testing samples

- Site accident/handling damage

Visible Wastage (MT) = Weight of collected/weighed scrap and rejected material

9.2 Invisible (Uncountable) Wastage

Real, but not collectible or weighable:

- Mill scale loss — surface scale flaking during handling and oxidation

- Cutting/kerf loss — the sliver lost at every cut line

- Bending loss — minor distortion at bend points

- Fines/dust during cutting or grinding

- Handling loss across multiple transfers (truck → store → work front → fixing)

Because none of this can be physically weighed, no contractor is asked to prove it with a weighbridge slip. Instead, a standard permissible wastage percentage is allowed — a small, universally accepted margin for unavoidable loss during handling and fixing, regardless of how careful the contractor is.

9.3 Standard Permissible Wastage in Steel Reconciliation

Most Indian contract specifications allow a total permissible wastage of 2% to 3% on theoretical quantity (always confirm against your specific contract; complex bending like chimneys/silos may justify a higher figure). This percentage covers both unrecoverable visible scrap and the entire invisible wastage category combined — it is not an additional allowance on top of visible scrap.

Excess Wastage Calculation — The Final Commercial Step in Steel Reconciliation

10.1 The Master Steel Reconciliation Equation

Net Issued Qty = Theoretical Qty + Permissible Wastage + Excess Wastage − Reusable Cut Pieces (utilized) + Unbilled/Balance in Hand

Rearranged to isolate excess wastage:

Excess Wastage = Net Issued Qty − Theoretical Qty − Permissible Wastage Allowance − Balance Stock in Hand

Permissible Wastage Allowance (MT) = Theoretical Quantity (MT) × Permissible Wastage % ÷ 100

10.2 Worked Example — Complete Steel Reconciliation Calculation

Given (16mm dia):

- Gross Issued Quantity = 103.00 MT

- Rolling Margin (tested) = +3%

- Theoretical Quantity (BBS) = 96.00 MT

- Permissible Wastage (contract) = 3%

- Balance stock in hand (verified, unused) = 1.20 MT

Step 1 — Net Issued Quantity:

Net Issued Quantity = 103.00 ÷ 1.03 = 100.00 MT

Step 2 — Permissible Wastage Allowance:

96.00 × 3 ÷ 100 = 2.88 MT

Step 3 — Expected Total Consumption:

96.00 + 2.88 = 98.88 MT

Step 4 — Actual Quantity Consumed:

100.00 − 1.20 = 98.80 MT

Step 5 — Excess/(Saving) Wastage:

98.80 − 98.88 = −0.08 MT (a saving; no recovery due)

If actual consumption had instead been 101.50 MT:

Excess Wastage = 101.50 − 98.88 = 2.62 MT

Recovery Amount = Excess Wastage (MT) × Issue Rate of Steel (₹/MT)

10.3 A Note on Fairness in Steel Reconciliation

Excess wastage should never be calculated in isolation — always cross-check rolling margin direction, cut-piece reuse, and unbilled/balance stock first. A steel reconciliation that skips any of these will almost always show an inflated, unfair figure against the contractor, and that is precisely what leads to prolonged disputes at project closure.

Steel Reconciliation Statement Format (Table)

Below is the complete, dia-wise steel reconciliation format used to consolidate everything covered in this guide into one auditable statement:

| Sr. | Particulars | Formula / Basis | Unit | Value (16mm eg.) |

| 1 | Opening Balance (Stock brought forward) | Carried from previous period | MT | 0.00 |

| 2 | Add: Total Received at Site (GRN Cumulative) | Σ Accepted Weight per GRN | MT | 103.00 |

| 3 | Total Available Quantity | (1) + (2) | MT | 103.00 |

| 4 | Gross Issued Quantity to Contractor | Σ Quantity per MIS | MT | 103.00 |

| 5 | Rolling Margin (tested, dia-wise) | (Actual − Theoretical Unit Wt) ÷ Theoretical Unit Wt × 100 | % | +3.00 |

| 6 | Net Issued Quantity (Rolling Margin Corrected) | (4) ÷ (1 + Rolling Margin%) | MT | 100.00 |

| 7 | Less: Balance Stock Lying Unused (verified) | Physical verification | MT | 1.20 |

| 8 | Actual Quantity Consumed | (6) − (7) | MT | 98.80 |

| 9 | Theoretical Quantity as per BBS | Σ (Length × D²/162) | MT | 96.00 |

| 10 | Add: Extra Steel (Chairs/Spacers/Extra Laps) | Reconciled, not billed | MT | Site-specific |

| 11 | Permissible Wastage Allowance | (9) × Permissible Wastage % | MT | 2.88 |

| 12 | Total Expected Consumption | (9) + (10) + (11) | MT | 98.88 |

| 13 | Excess / (Saving) Wastage | (8) − (12) | MT | (0.08) |

| 14 | Recovery Amount (if Item 13 is positive) | (13) × Issue Rate (₹/MT) | ₹ | Nil |

| 15 | Unbilled Quantity (Fixed, not yet certified) | Physical + measurement cut-off | MT | Site-specific |

| 16 | Closing Balance (Carried Forward) | Balance stock not yet consumed | MT | 1.20 |

Prepare this table dia-wise for every diameter used on the project, then consolidate into a summary sheet for the final steel reconciliation statement.

Closing Thoughts on Steel Reconciliation

Steel reconciliation is not just an accounting exercise — it is a discipline that begins the day the first truck rolls into site and continues until the very last bill is certified. Every stage — delivery verification, GRN discipline, dia-wise issue tracking, rolling margin correction, BBS-based theoretical calculation, an honest split between cut pieces and scrap, and a clear separation of visible from invisible wastage — builds on the one before it. Skip any single stage, and the final steel reconciliation statement becomes a source of dispute rather than a tool of clarity.

In my experience, the projects where steel reconciliation goes smoothly at closure are invariably the ones where this discipline was built in from day one — not assembled retrospectively from incomplete records. I hope this guide gives you that same structured foundation, whether you are preparing your first MRS or refining a process you have run for years.

For More Blogs follow the below links

Basic Rate Difference ( BRD ) – Common Mistakes and Billing & Audit Red Flags

")

")