Billing Process in Construction Projects: The Complete Guide Every Civil Engineer Must Know & Improve in 2026

The Problem No One Talks About Openly

If you have ever stood at a construction site on the last working day of the month, surrounded by measurement books, rate analysis sheets, deviation registers, and a contractor’s billing executive who is already three days behind schedule, you already know the chaos that lives inside the billing process in construction projects. It is not a clean, linear process. It is part technical verification, part legal documentation, part financial negotiation, and part institutional memory. And yet, in most engineering colleges across India, this entire subject gets maybe two lectures if it gets any at all.

I have spent years working at this exact intersection of civil engineering and construction finance. I have prepared RA bills for government infrastructure contracts, verified billing documents on large PMC-managed projects in Mumbai, dealt with CAG audit objections, and supported contractors in resolving billing disputes. What I have learned sometimes painfully is that the billing process in construction projects is not just paperwork. It is the financial nervous system of every project, and when it malfunctions, the consequences ripple across costs, timelines, professional reputations, and sometimes even legal proceedings.

This guide is my attempt to put everything I know into one place written in plain language but with the technical depth that working civil engineers actually need. Whether you are a junior engineer preparing your first RA bill, a project manager reviewing contractor claims, a PMC professional seeking audit-ready practices, or a contractor’s billing engineer trying to understand what gets flagged and why this guide is written for you. And because I am writing this specifically for the Indian construction ecosystem, with its own unique blend of DSR rates, government tender norms, GST compliance, BOCW obligations, and statutory audit culture every section reflects real-world Indian practice, with specific Mumbai and Maharashtra references where relevant.

Why the Billing Process in Construction Projects Matters More Than You Think

1. Cost Overruns Begin with Billing Gaps

Every project manager will tell you that cost overruns happen because of scope changes, material price escalation, or contractor inefficiency. That is true but what they often understate is how much financial leakage happens quietly, through billing errors that are never caught until it is too late. On a ₹40 crore civil works project, a consistent overbilling pattern of just 1.5% per RA bill across 18 months translates to ₹60 lakhs of financial exposure. That money does not vanish dramatically. It seeps out through wrong quantity abstracts, unchecked extra items, unapplied recoveries, and premature retention releases.

The billing process in construction projects is the first and most important line of defense against cost leakage. And that defense works only when engineers at every level JE, AE, EE, PM understand exactly what to verify, at what stage, and why.

2. Audit Risk is a Career Reality in Indian Construction

Government-funded construction projects in India, those executed by CPWD, NHAI, PWD, MMRDA, Smart City SPVs, municipal corporations, housing boards are subject to statutory audit by the Comptroller and Auditor General of India (CAG) or internal audit wings. An improperly certified RA bill is not a minor clerical oversight. It is a professional liability for the engineer who signed the passing certificate. CAG audit objections called Inspection Reports (IRs) result in recovery notices, departmental inquiries, and in serious cases, criminal proceedings under the Prevention of Corruption Act.

I have seen excellent site engineers competent, hardworking professionals face career-altering consequences because they certified bills without understanding what they were certifying. This guide will give you the knowledge to certify with confidence, because you will know exactly what each line item means and what the audit team will look for.

3. Career Relevance in India’s Infrastructure Decade

India is in the middle of a historic infrastructure push. The National Infrastructure Pipeline (NIP) envisions over ₹111 lakh crore of investment across roads, railways, ports, airports, urban infrastructure, and industrial corridors over the coming years. RERA has transformed real estate project finance. Smart Cities are demanding digital billing transparency. NHAI projects now require geo-tagged measurements and digital bill submissions. The civil engineer who understands only design and execution is already falling behind. The engineer who combines site knowledge with billing proficiency, audit awareness, and contract management capability is the professional that clients, PMC firms, and contractors are genuinely competing to hire.

What Is the Billing Process in Construction Projects?

The billing process in construction projects is the structured, document-driven procedure through which a contractor formally claims payment for work physically completed at site, and the client or their authorized engineer verifies that claim, certifies it as accurate and legitimate, and initiates financial payment in accordance with the terms of the construction contract.

Put simply: work happens, it is measured, a bill is prepared, it is checked, and payment follows. But between each of those verbs lies a world of technical judgment, legal obligation, and documentary discipline that this guide unpacks completely.

The Governing Documents of Construction Billing

The billing process does not exist in isolation. Every claim and every verification must be traceable back to one or more of these foundational contract documents:

- The Tender Document, including the Notice Inviting Tender (NIT) and all corrigenda

- The Bill of Quantities (BOQ), with scheduled rates for every payable item

- The General Conditions of Contract (GCC) and Special Conditions of Contract (SCC)

- Approved Drawings and Technical Specifications

- Deviation / Variation Orders and Technical Sanctions for extra items

- Price Variation (Escalation) clauses and applicable index data

In international contracts, the equivalent framework is provided by FIDIC (Fédération Internationale des Ingénieurs-Conseils) — primarily the Red Book (Construction Contracts), Yellow Book (Plant & Design-Build), or Silver Book (EPC/Turnkey) — which I will address in detail in the global comparison section of this guide.

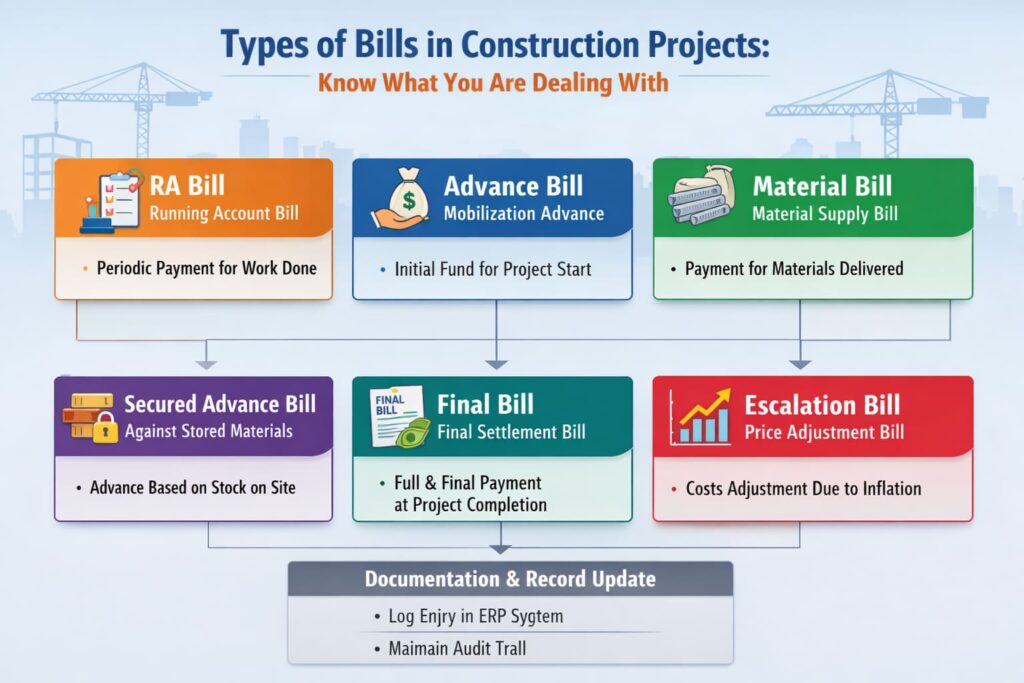

Types of Bills in Construction Projects: Know What You Are Dealing With

Before diving into the process, a billing professional must clearly understand the categories of bills that appear across a project’s financial lifecycle. Each type has its own purpose, documentation requirement, and approval pathway.

| Bill Type | When Raised | Key Features | Audit Sensitivity |

| Running Account (RA) Bill | Periodically during execution (monthly / milestone) | Cumulative format; most frequent; governed by MB entries | HIGH — quantity verification is core |

| First & Final Bill | Small works; after completion | Single bill covering entire scope | MEDIUM — completion must be certified |

| Final Bill | After full project completion | Closes financial account; NCC signed | VERY HIGH — settlement of all deviations |

| Mobilization / Secured Advance Bill | Early contract stage | Recoverable from RA bills; BG required | HIGH — recovery tracking must be exact |

| Extra Item Bill / Deviation Statement | When scope exceeds BOQ | Requires prior Technical Sanction + rate analysis | VERY HIGH — most common audit objection |

| Price Variation (Escalation) Bill | Long-duration contracts | Index-based formula calculation | HIGH — formula and index selection scrutinized |

Step-by-Step Billing Process in Construction Projects: The Complete Workflow

I am going to walk you through the complete billing process as it functions in a typical Indian government or PMC-managed construction project. I will note where private sector or FIDIC-based projects differ. This is a seven-step workflow and every step matters.

STEP 1 Joint Site Measurement and Measurement Book (MB) Recording

The entire billing edifice rests on one foundation: the Measurement Book. In Indian government construction contracts, the MB is a legally recognized official record. Every payment, every audit verification, every dispute resolution traces back to what is or is not recorded in the MB. There is no billing without measurement, and there is no credible measurement without a properly maintained MB.

Who measures: The Junior Engineer (JE) or Sub-Engineer from the client or PMC side, always in the presence of the contractor’s authorized site representative. Both parties must be present, a unilaterally recorded MB entry is an immediate audit red flag.

What is measured: Every BOQ item for which payment is to be claimed earthwork, concrete, formwork, reinforcement, masonry, plastering, flooring, external works, services. Each measurement corresponds directly to a specific BOQ line item.

Measurement standard: IS: 1200 (Method of Measurement of Building and Civil Engineering Works) is the standard reference in Indian contracts. MoRTH specifications apply for road and bridge works. CPWD Specifications apply for building works under CPWD contracts. Mumbai-specific municipal works often follow MCGM or MMRDA tender specifications, which incorporate IS standards with project-specific amendments.

MB discipline: Entries must be in ink. No overwriting corrections are made with a single horizontal strike-through followed by the correcting officer’s initials and date. Every measured structure must be accompanied by a dimensioned sketch. MB page numbers and references must be noted clearly in every bill abstract.

In private real estate projects in Mumbai those by Godrej Properties, Lodha, Oberoi Realty, or L&T Realty digital measurement records or Site Instruction Books may replace paper MBs, but the principle of cross-verified, jointly-recorded measurements remains non-negotiable.

STEP 2 Abstract of Cost Preparation

Once measurements are recorded and both parties have signed the MB, the billing engineer (typically from the contractor’s side, under supervision of the PMC/client) prepares the Abstract of Cost. This is the bridge between physical measurements and financial figures.

The abstract maps each MB measurement to its corresponding BOQ item number, multiplies the quantity by the contract rate, and generates the line-item amount. The abstract is always cumulative it shows total quantities from Day 1 of the project to the current billing date. The difference between this bill’s cumulative total and the previous RA bill’s cumulative total gives the net quantity and value for the current billing period.

| Sr. No. | Item Description | BOQ Ref. | Unit | Qty (MB Ref.) | Contract Rate (₹) | Amount (₹) |

| 1 | PCC 1:4:8 in Foundation | Item 1.2 | Cum | 45.60 (MB-3, p.12) | 4,200 | 1,91,520 |

| 2 | RCC M25 in Columns | Item 2.3 | Cum | 28.75 (MB-3, p.14) | 7,800 | 2,24,250 |

| 3 | TMT Steel Fe-500 in Columns | Item 2.4 | MT | 2.85 (MB-3, p.16) | 68,000 | 1,93,800 |

| 4 | Brick Masonry in Superstructure | Item 3.1 | Cum | 38.20 (MB-3, p.18) | 3,600 | 1,37,520 |

| Gross Total (Current RA Bill) | ₹7,47,090 |

STEP 3 RA Bill Preparation with Full Recovery Statement

With the abstract complete, the formal Running Account Bill is assembled. This document has a defined structure in government contracts, and any deviation from that structure is a reason for the bill to be returned. Let me walk through each component:

Bill Header: Name of work, agreement number, contractor’s name and registration details, RA bill number, billing period (from–to dates), and name of the certifying officer.

Gross Amount: Total value of work done as per the Abstract of Cost.

Recoveries (Deductions): This is where most billing errors hide. Every applicable deduction must be computed correctly and applied.

| Recovery Item | Rate / Basis | Legal Authority | Common Mistake |

| Income Tax (TDS) | 1% (individuals) or 2% (companies) of gross | Section 194C, Income Tax Act | Applying wrong slab or missing entirely |

| GST TDS | 2% of taxable value (govt. projects) | Section 51, CGST Act 2017 | Not deducting for contracts that qualify |

| Labour Welfare Cess (BOCW) | 1% of construction cost | BOCW Welfare Cess Act, 1996 | Routinely missed — top audit objection |

| Mobilization Advance Recovery | As per agreement schedule | Contract Agreement clause | Recovery installments skipped or delayed |

| Secured Advance Recovery | Material advance as per clause | Contract Agreement clause | Recovery not tracked against advances given |

| Retention Money | Typically 5% of gross bill amount | Contract GCC clause | Not applied or released prematurely |

| Penalty / LD (if applicable) | As per contract — daily rate × delay | Contract clause; requires prior notice | Applied without formal LD notice — legally defective |

GST Note for Mumbai / Maharashtra Projects: Construction services are generally taxable at 18% GST (HSN 9954). However, government civil works contracts and affordable housing projects under PMAY may attract 12% GST subject to specific notifications. Contractors must raise a GST Tax Invoice alongside every RA bill. In Maharashtra, GSTIN registration, HSN/SAC coding, and GSTR-1 reconciliation are subject to spot checks during audit. Errors in GST invoicing affect Input Tax Credit (ITC) for the client making GST compliance a shared responsibility, not just the contractor’s problem.

Net Payable Formula: Net Payable = Gross Amount − (Income Tax TDS + GST TDS + BOCW Cess + Mobilization Advance Recovery + Secured Advance Recovery + Other Deductions) − Retention Money

STEP 4 Bill Register (BRD) Entry and Formal Submission

Once prepared, the RA bill is formally submitted to the client or PMC office and entered into the Bill Register / Bill Receipt Document (BRD). This is the official log of all bills submitted against the contract. Every entry gets a unique receipt number and date-stamp and this record is the first document an auditor asks for when reviewing a project.

Supporting documents submitted with the bill include: original RA bill in triplicate (for government contracts), all referenced MB page numbers, GST Tax Invoice, material test certificates for specification-controlled items (concrete cube reports, brick test results, bitumen test reports), progress photographs with geotagging and date-stamping (mandatory in most NHAI and MMRDA contracts), insurance certificates if contractually required, and labour attendance records for labour-based contracts.

STEP 5 Technical Verification by Site Engineer

This is the first formal checkpoint and arguably the most important one for preventing billing errors from becoming certified mistakes. The Junior Engineer or Assistant Engineer from the client or PMC side conducts the technical verification against the following checklist:

- Are all quantities in the bill consistent with and traceable to specific MB entries?

- Is the work actually physically complete as claimed, or is it partially done?

- Are all items billed within the defined scope of the BOQ?

- Do material specifications match what was used on site (e.g., concrete grade, steel grade)?

- Are quality control documents (cube test reports, material test certificates) available and matched to the billing period?

- Are measurements taken as per IS: 1200 or the applicable method of measurement?

- Is there any billing of work that fails the specification criteria?

The site engineer records their verification findings in writing, certifies the technical accuracy of the bill with remarks, and passes it up to the next level of the approval hierarchy. A verbal or implied certification is not sufficient written remarks with signature and date are the minimum standard.

STEP 6 Engineer-in-Charge Certification (Passing Certificate)

The Project Manager, Executive Engineer (EE), or Engineer-in-Charge carries out the second and determinative level of review. This certification called the Passing Certificate in CPWD contracts and the Interim Payment Certificate (IPC) in FIDIC contracts carries full legal and financial weight. The person who issues this certificate is personally accountable for its accuracy.

At this level, the critical questions are contractual rather than purely technical: Do any items in this bill exceed BOQ quantities without a sanctioned deviation statement? Are extra items billed without prior technical sanction and approved rate analysis? Is the escalation claim computed correctly using the formula and indices specified in the contract? Have all mandatory deductions been applied correctly? Is the retention percentage correctly withheld?

After satisfactory review, the Engineer-in-Charge issues the Passing Certificate. In CPWD contracts, this is the trigger for accounts processing. In FIDIC contracts, the issuance of the IPC starts the 28-day payment clock.

STEP 7 Accounts Processing and Payment Release

The certified bill moves to the Finance / Accounts department for financial processing. The accounts team verifies budget availability (a real and frequent bottleneck in government projects), confirms TDS deduction under the correct provision, verifies GST TDS compliance, checks bank guarantee validity (if mobilization advance has been extended), and prepares the payment voucher. Payment is then released via RTGS/NEFT or demand draft to the contractor’s registered bank account.

In Indian government contracts, the payment period after certification is typically 28 to 30 days as per GCC. In MMRDA-managed projects in Mumbai, digital bill tracking systems allow contractors to monitor bill status in real-time. In private real estate projects, RERA mandates that developers release payments as per the approved escrow-linked schedule, with construction-linked payment milestones governing when specific bills can be raised.

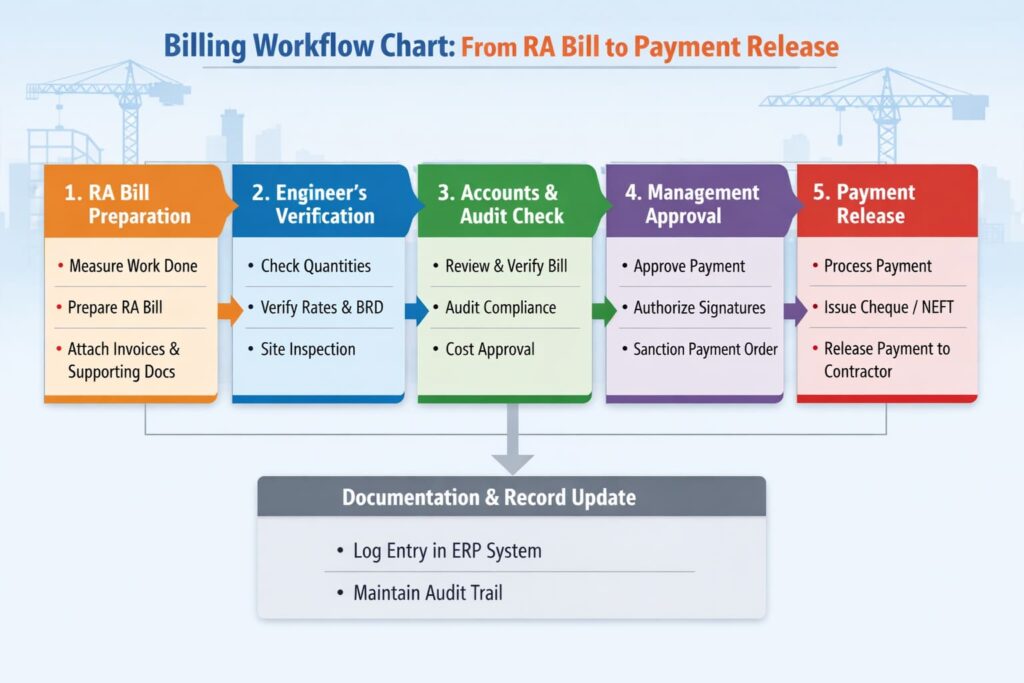

Billing Workflow Chart: From RA Bill to Payment Release

The following chart shows the complete flow of the billing process in construction projects — from the first site measurement to final payment credit in the contractor’s account.

| CONSTRUCTION SITE — WORK EXECUTION |

| ↓ Joint Measurement at site (JE + Contractor Representative) |

| STEP 1: Measurement Book (MB) Recording |

| ↓ Signed by both parties | Sketches & dimensions noted | IS:1200 standard |

| STEP 2: Abstract of Cost Preparation |

| ↓ BOQ item mapping | Quantity × Rate | Cumulative format |

| STEP 3: RA Bill + GST Tax Invoice Preparation |

| ↓ Recovery statement computed | Net payable calculated |

| STEP 4: Bill Register (BRD) Entry & Submission |

| ↓ Unique receipt number assigned | Supporting docs attached |

| STEP 5: Technical Verification — Site Engineer / JE |

| ↓ MB vs Bill quantity check | Quality docs verified |

| DISCREPANCY FOUND? ← → APPROVED |

| ↓ Return to Contractor ↓ |

| STEP 6: Engineer-in-Charge Certification / Passing Certificate |

| ↓ Contractual review | Deviation & extra item check | Legal compliance |

| STEP 7: Accounts Processing |

| ↓ TDS | GST TDS | Budget check | BG validity | Payment voucher |

| PAYMENT RELEASED — RTGS/NEFT within 28 days of Certification |

Real Project Scenarios: Billing in Action

Case Study 1 — Storm Water Drain & Road Improvement, Western Mumbai Suburb

Contract Value: ₹8.5 crore | Duration: 18 months | Client: Municipal Authority | PMC: Private consultancy | Contractor: Medium-scale civil contractor.

Month 3 — The Measurement Discrepancy Crisis The contractor submitted RA Bill No. 1 for ₹1.2 crore gross. The site engineer during technical verification found that the bill claimed 380 cubic meters of earthwork excavation. The Measurement Book, however, recorded only 310 cubic meters. The contractor’s billing team had used estimated quantities, not measured ones.

The discrepancy of 70 cubic meters, at ₹320 per cubic meter, amounted to ₹22,400. That is a small number in isolation but the principle it revealed was enormous. If estimated quantities were being used for earthwork, what was happening for concrete and reinforcement? The bill was returned with a formal discrepancy note. Joint re-measurement was carried out by the JE and contractor’s site supervisor. MB entries were corrected with dimensioned sketches. The corrected bill was cleared within 12 working days.

Key Learning: Never bill from estimates. Every quantity in every RA bill must trace to a specific MB entry, with the page reference noted in the abstract. This is not bureaucratic formality, it is the only protection an engineer has when the auditor arrives.

Case Study 2 — Extra Item Billing Without Sanction

On the same project, by Month 9, an unexpected soil condition required an additional layer of geotextile fabric under the drain bed, an item not present in the original BOQ. The contractor executed the work without prior discussion and included it in RA Bill No. 5 at a self-quoted rate.

The certifying engineer flagged three specific problems: No Technical Sanction had been obtained from the competent authority before executing the extra item. The rate had not been analyzed using Market Rate + 10% contractor’s profit the standard for extra items in most government contracts. Including an unsanctioned item in an RA bill is a violation of the GCC that results in automatic audit objection.

The extra item was removed from RA Bill No. 5. A formal Rate Analysis was prepared supported by three market quotations and cross-referenced with the applicable Schedule of Rates. Technical Sanction was obtained from the Superintending Engineer (SE) level. The item was included in RA Bill No. 6 after proper authorization.

Key Learning: No extra item regardless of how genuinely necessary it is, should ever be billed without prior Technical Sanction and an approved Rate Analysis document. Site pressure will always push for ‘do now, sanction later.’ The engineer’s job is to hold the line.

Case Study 3 — GST Mismatch in a RERA-Registered Mumbai Residential Project

Project: High-rise residential tower in Thane. Developer (client): Listed real estate company. Contractor: Specialized RCC contractor. Contract Value: ₹22 crore. The contractor applied 18% GST on all RA bills. The client’s tax team raised a flag in Month 6 the project qualified for the 12% GST rate under the notification applicable to residential projects under RERA, subject to the condition that Input Tax Credit was not claimed.

The contractor had to reverse the excess GST already paid for the first five bills, file amendments in GSTR-1, issue revised Tax Invoices, and recover the differential from GSTN a process that took nearly three months and involved the contractor’s CA, the client’s finance team, and the GST practitioner. Billing was effectively stalled during this period, causing contractor cash flow stress.

Key Learning: In every Mumbai / Maharashtra construction project, the applicable GST rate must be established and legally confirmed before the first RA bill is raised, not after five bills have been submitted. When in doubt, get a written legal opinion. The cost of a CA consultation is negligible compared to the cost of a GST revision exercise.

Common Billing Mistakes and Audit Red Flags: What Engineers Most Often Miss

The following are not hypothetical errors. Every one of these has appeared in actual audit objections or billing disputes across Indian construction projects. I have organized them with the specific audit trigger and the practical fix.

| Mistake | Audit Red Flag | Fix / Best Practice |

| Billing incomplete work as 100% done | Site photos dated on billing date show incomplete work; physical inspection reveals mismatch | Engineer must physically verify completion before certifying. Attach dated, geotagged progress photos. |

| Duplicate billing of quantities across RA bills | Cumulative quantities in current bill exceed actual site measurements | Maintain a running quantity tally per BOQ item. Update after every bill. Never rely on memory. |

| Wrong item classification / higher-grade billing | Concrete pour registers, delivery challans show different grade than billed | Billing must match actual specification. Rate upgrades need a formal variation order. |

| Billing without material test reports | Quality certificates unavailable or dated outside billing period | Link quality test register to MB entries. No test result = no billing for that item. |

| Incorrect GST rate applied | GSTN mismatches in ITC reconciliation; audit of GST returns | Confirm applicable rate legally before first bill. Maintain HSN/SAC register. |

| BOCW Cess not deducted | Standard statutory audit objection in almost all government projects | Include 1% BOCW Cess as a fixed recovery in every RA bill template. Maintain cess register. |

| Extra items billed without Technical Sanction | Most common and severe audit objection; results in full recovery + interest | Zero tolerance: no extra item work commences without TS. Engineer must refuse to certify without it. |

| Retention released before DLP expiry | Retention released without physical DLP inspection completion certificate | Maintain a Retention Release Register with DLP expiry dates per contract. BG substitution documented. |

| Advance recovery skipped or delayed | Recovery register shows gaps; contractor effectively given interest-free loan | Use a dedicated Advance Recovery Tracker. Automate recovery deductions in the bill template. |

| MB entries not signed or counter-signed | MB entries without joint signatures treated as unilateral — not admissible in audit | Enforce joint signing discipline at the time of measurement, not later. |

Tools and Techniques for the Billing Process in Construction Projects

Software and Digital Tools

Microsoft Excel (Custom Billing Templates): The most widely used tool in Indian construction billing at all project scales. A well-built Excel workbook with linked sheets for MB abstract, cumulative quantity tracker, recovery statement, and bill summary can prevent most manual errors. Pivot tables for quantity cross-verification and conditional formatting to flag quantity overruns are standard features in professionally designed billing templates.

ERP Systems — SAP, Oracle, Primavera: Used by large contractors (L&T, Shapoorji Pallonji, Tata Projects) and PMC firms (AECOM, Mott MacDonald, Jacobs). These platforms link billing to project scheduling, procurement, and cost accounting — enabling real-time cost-to-completion projections and automated bill generation against approved BOQ items.

CCS Candy (Benchmark Estimating / CostX): Popular in Southern Africa and increasingly present in large Indian contracts through international joint ventures. Excellent for BOQ-based cost control and quantity takeoff with direct linkage to billing.

PMIS Platforms (NHAI, MMRDA, Smart City SPVs): Many large government authorities in India now operate proprietary Project Management Information Systems that require digital bill submission with uploaded MB scans, quality certificates, and geo-tagged photographs. NHAI’s INFRACON platform and MMRDA’s project portal are examples where billing transparency is being institutionalized.

BuildSmart and Asite: Construction-specific platforms gaining traction in India for contractor-side billing management, document control, and digital workflow approvals — particularly on projects with PMC oversight where turnaround times matter.

Essential Billing Formulas Every Engineer Must Know

| Formula | Expression | Notes |

| Gross Bill Amount | Σ (Qty of Item × Contract Rate) | Cumulative from project start |

| Net Amount After Recoveries | Gross − (TDS + GST TDS + BOCW + Mob. Rec. + Sec. Adv. Rec. + Other) | All deductions must be applied |

| Payment Due This Bill | Net − Retention Amount | Retention = 5% of Gross typically |

| Retention Amount | Retention % × Gross Amount | Withheld till DLP expiry |

| BOCW Cess | 1% × Total Construction Cost billed | Under BOCW Welfare Cess Act |

| Escalation (Illustrative) | Paid Amount × [(New Index − Base Index) / Base Index] × Weightage | Formula varies by contract |

| Extra Item Rate | Market Rate + 10% Contractor’s Profit | Subject to negotiation per contract |

| Deviation Allowance | BOQ Qty × (Permissible Deviation % / 100) | Typically ±25% in CPWD contracts |

Pre-Submission Billing Checklist

| RA BILL PRE-SUBMISSION CHECKLIST — Civil Billing Specialist Standard | |

| ☐ | All MB entries for this billing period are complete, jointly signed, and page references noted |

| ☐ | Abstract quantities have been verified against MB entries line by line |

| ☐ | Cumulative quantities checked against all previous RA bills — no duplicates |

| ☐ | No BOQ item exceeds permissible quantity without a sanctioned deviation statement |

| ☐ | All extra items included have a Technical Sanction order and approved Rate Analysis |

| ☐ | GST Tax Invoice prepared with correct HSN/SAC code and applicable rate (12% or 18%) |

| ☐ | GST rate verified against contract category and applicable GST notification |

| ☐ | All mandatory recoveries computed: TDS, GST TDS, BOCW Cess, advances, retention |

| ☐ | Retention percentage correctly withheld from gross amount |

| ☐ | Supporting documents attached: quality test reports, progress photos, delivery challans |

| ☐ | MB entry photographs or scans appended as annexure (for digital submissions) |

| ☐ | Bill signed by contractor’s authorized signatory with date and seal |

| ☐ | Bill Register entry date and receipt number confirmed before certifying |

| ☐ | RERA compliance checked for real estate projects (payment linked to approved milestone) |

| ☐ | Labour welfare cess deduction register updated after deduction |

Global Comparison: Indian Billing Norms vs FIDIC International Standards

One quality that distinguishes a truly senior billing professional is the ability to move fluently between Indian contract frameworks and international standards. If you work with multinational PMC firms, World Bank or ADB-funded projects, or international joint ventures, FIDIC will be your contract framework. Understanding how it differs from Indian practice is essential.

| Parameter | Indian Government Contracts (CPWD/PWD/NHAI) | FIDIC Red Book (International) |

| Billing Instrument | Running Account (RA) Bill | Interim Payment Certificate (IPC) — Clause 14.3 |

| Measurement Document | Measurement Book (MB) — jointly signed | Engineer’s determination or Contractor’s Statement |

| Billing Frequency | Monthly or milestone-based | Monthly (Clause 14.3) |

| Certification Timeline | 14–28 days after submission (contract-specific) | 28 days from Payment Statement date (Clause 14.6) |

| Payment Timeline | 28–30 days from certification (contract-specific) | 56 days from Payment Statement date (Clause 14.7) |

| Late Payment | Interest provisions vary; often absent in state PWD contracts | Financing charges apply automatically (Clause 14.8) |

| Retention | 5% per bill; released after DLP inspection | 5–10%; released in two tranches — 50% on TOC, 50% after DLP (Clause 14.9) |

| Extra Items / Variations | Technical Sanction + Rate Analysis required | Engineer’s Instruction + Variation Order (Clause 13) |

| Dispute Resolution | Arbitration under Arbitration & Conciliation Act, 1996 | DAAB first, then amicable settlement, then arbitration |

| Price Escalation | WPI/CPI-based formula in contract schedule | Formula-based with defined indices (Clause 13.8) |

| Final Account | No Claim Certificate + Final Bill | Final Payment Certificate (Clause 14.13) |

| Engineer’s Role | Authorized Agent / Engineer-in-Charge; client employee | Independent Engineer; quasi-arbitrator under contract |

| Advance Payment | Mobilization/Secured Advance per contract clause | Advance Payment with bank guarantee (Clause 14.2) |

| Performance Security | Bank Guarantee / FDR (5–10% of contract value) | Performance Security with defined format (Clause 4.2) |

Key Insight for Indian Engineers: Under FIDIC, the Engineer’s role is quasi-judicial, they must act impartially between the contractor and the employer. In Indian government contracts, the Engineer-in-Charge is effectively the client’s employee. This fundamental difference in the Engineer’s position affects how disputes are raised, how variations are valued, and how billing objections are resolved. Engineers moving from Indian government contracts to FIDIC-based projects must internalize this distinction.

Another critical FIDIC concept that is gaining relevance in India through World Bank and ADB-funded projects is the Dispute Avoidance/Adjudication Board (DAAB), a standing panel of neutral experts who resolve disputes in real time during project execution, before they escalate to arbitration. India’s arbitration framework does not yet have an equivalent to the DAAB in standard government contracts, though some large private projects have begun adopting similar dispute review panels.

Audit-Ready Billing: The Angle Most Engineering Blogs Completely Miss

I want to spend serious time on this section because it is what separates a competent billing engineer from one who is genuinely audit-proof. Most construction billing guides cover the process. Almost none cover what happens when the auditors arrive which they always do, eventually.

What Statutory Auditors Actually Look For

CAG audit teams, internal audit wings, and third-party inspectors operate from a checklist of standard red flags that have been refined over decades of government project auditing. Here is what they specifically examine and what you must be prepared to defend:

MB Authenticity and Completeness: Auditors are trained to spot recently filled MB entries passed off as contemporaneous records. They look at ink consistency, signature freshness, sequential page usage, and whether sketches match the described structure. Blank spaces in MBs, entries without counter-signatures, and MBs with entries that do not correspond to site photographs are all flagged as suspicious.

Rate Reasonableness for Extra Items: Every extra item rate is compared against DSR (Delhi Schedule of Rates, CPWD), MoRTH Schedule, or local schedule of rates. A rate that exceeds the applicable schedule rate without documented justification is flagged as excess payment. The rate analysis document must explicitly show: material cost + labour cost + tools & plant + contractor’s profit (typically 10%) + overhead.

Deviation Statement Compliance: Auditors compare total billed quantities per BOQ item against the tendered quantity. Where excess is detected, they check whether a deviation statement was sanctioned and whether the competent authority (SE, CE, or equivalent) approved the excess before it was billed. Billing at deviated quantities without sanction is one of the most heavily penalized audit findings.

Quality Evidence for Specification-Controlled Items: For concrete work, auditors cross-reference concrete cube test reports (28-day strength) with the billing period and the volumes billed. If the test reports are unavailable, are from a non-accredited lab, or do not cover the quantities billed, the entire concrete billing for that period is suspect. For structural steel, mill test certificates and delivery challans are the primary evidence.

Advance Recovery Compliance: The advance recovery register is compared against the payment advice statements for each RA bill. Any gap in recovery any RA bill where recovery was not applied when it should have been — is treated as an unauthorized extension of interest-free credit to the contractor, and the notional interest loss is quantified as a financial irregularity.

Retention and DLP Compliance: Retention release is cross-checked against the project completion certificate date and the DLP end date. If retention was released before the DLP expired without substitution by a bank guarantee of equivalent value — this is a finding. The responsible officer is expected to explain and justify the decision.

The Bill Audit File: My Recommended Standard

For every RA bill certified, I recommend maintaining what I call a Bill Audit File, a dedicated physical or digital folder that contains every document that was reviewed before certification. The content of this file should be:

| Document | Purpose in Audit | Retention Period |

| Original RA Bill (signed copy) | Primary financial record | Till project closure + 5 years minimum |

| MB references (scan or physical) | Quantity verification backbone | Till project closure + 5 years minimum |

| Abstract of Cost | Links MB to bill amounts | Till project closure + 5 years minimum |

| GST Tax Invoice | Tax compliance verification | 6 years (GST law requirement) |

| Material test certificates | Quality compliance evidence | Till project closure + 5 years minimum |

| Extra Item TS order (if applicable) | Authorisation for non-BOQ item | Permanent record — never dispose |

| Rate Analysis (for extra items) | Justification for approved rate | Permanent record — never dispose |

| Deviation Statement (if applicable) | Authorisation for quantity excess | Permanent record — never dispose |

| Progress photographs (dated) | Visual evidence of work completion | Till project closure + 3 years minimum |

| Recovery computation worksheet | Deduction compliance proof | Till project closure + 5 years minimum |

| Advance recovery ledger extract | Running track of advance status | Till project closure + 5 years minimum |

Rule of Thumb: If an audit team asks for any document related to a certified bill, you should be able to retrieve it within five minutes. If you cannot, the documentation process has failed, regardless of whether the underlying work was done correctly.

Best Practices to Prevent Cost Leakage in Construction Billing

Cost leakage in construction projects is rarely dramatic. It is usually slow, quiet, and systemic. Here are the practices that consistently prevent it:

- Fix the Measurement Protocol Before Work Begins. At the project kickoff meeting, establish in writing: who measures, with what instruments, on which days of the month, following which IS standard. Both client and contractor representatives must be named. A measurement protocol agreed at the start eliminates 70% of later disputes.

- Implement a Quantity Control Register. For every BOQ item, maintain a running log showing: Tendered Quantity, Billed to Date | Balance | Status (Normal / Near Limit / Deviated). Update this after every RA bill. When any item approaches 80% of the tendered quantity, initiate the deviation statement process immediately not when the bill is already being prepared.

- Zero Tolerance on Unsanctioned Extra Items. This is not a guideline, it is a rule. No extra item work begins without Technical Sanction. No extra item is billed without approved Rate Analysis. The engineer who enforces this consistently will never face an audit objection on extra items.

- Integrate Billing with Quality Management. The quality control register and the MB are not separate documents, they should be parallel records. For specification-controlled items, the MB entry is made only after the quality test result is received. No test = no measurement = no billing.

- Use a Standardized Recovery Statement Template. Create a fixed template that automatically computes every applicable deduction TDS, GST TDS, BOCW Cess, advance recoveries, retention, when you enter the gross amount. This eliminates the risk of a forgotten deduction, which is both an audit objection and a financial loss to the project.

- Hold a Monthly Billing Review Meeting. Before any RA bill is formally submitted, hold a review meeting with the contractor’s billing team, the site engineer, and the PM. Go through the draft bill line by line. Catch errors in a collaborative environment not after the bill is in the certification pipeline. This single practice, consistently applied, transforms billing quality.

- Build a Retention Release Calendar. At project commencement, create a calendar entry for the DLP expiry date for every contract. Thirty days before expiry, initiate the DLP inspection process. Release retention only after a formal written DLP inspection report confirms that all defects have been attended to.

- Train the Contractor’s Billing Team. The most overlooked investment in construction project management. A half-day training session for the contractor’s billing executive at the start of a project covering MB discipline, recovery computation, GST invoicing, and extra item process prevents months of billing disputes and delays.

India and Mumbai-Specific Billing Norms: What Makes Our Context Unique

The billing process in construction projects in India operates within a regulatory and institutional environment that is distinctly different from any other country. Here are the key India-specific and Mumbai-specific factors that every billing professional must internalize:

CPWD Schedule of Rates (DSR): The Central Public Works Department publishes annual Delhi Schedule of Rates, the benchmark for rate analysis for extra items, deviation quantities, and comparative rate assessments in government construction projects across India. Many state PWDs publish their own SoRs. In Maharashtra, the Maharashtra PWD publishes the Maharashtra Schedule of Rates, and MMRDA projects reference both DSR and market rates for extra items.

MCGM and MMRDA Tender Norms: Municipal Corporation of Greater Mumbai (MCGM) and Mumbai Metropolitan Region Development Authority (MMRDA) have their own standard tender documents, GCC, and billing formats that differ from CPWD norms in specific ways, particularly around quality certification requirements, labour compliance norms, and submission formats. Engineers working on Mumbai civic infrastructure must be familiar with these authority-specific norms, not just generic government contract standards.

RERA Impact on Real Estate Billing: For real estate construction in Maharashtra, the Real Estate (Regulation and Development) Act, 2016 and the Maharashtra Real Estate Regulatory Authority (MahaRERA) regulate the payment structure between developers and contractors. Construction-linked payment plans must be registered, milestone definitions must be RERA-compliant, and funds must flow through designated escrow accounts. A contractor billing outside the RERA-registered milestone framework creates compliance risk for both parties.

Labour Welfare Cess (BOCW Act): Maharashtra is one of the most active states in BOCW Cess collection. The Maharashtra Building and Other Construction Workers Welfare Board (MBOCWWB) requires registration of all construction projects above ₹10 lakhs and regular deposit of the 1% cess deducted from contractor payments. Audit teams in Maharashtra specifically check BOCW cess deduction and deposit compliance for every project.

CAG Audit Culture: India’s CAG audit is one of the most rigorous performance audit systems in the world for public infrastructure spending. The CAG not only checks compliance, it evaluates value for money, efficiency of execution, and propriety of payments. Engineers who understand the CAG’s audit methodology which is publicly available in the CAG’s Audit Manual are better positioned to maintain audit-ready billing practices from day one.

Editor’s Pick

-

Read more: Standardized Excavation Measurement Benchmark – IS Code Explained

Read more: Standardized Excavation Measurement Benchmark – IS Code ExplainedStandardized Excavation Measurement Benchmark – IS Code Explained

on

-

Read more: Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

Read more: Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026Bar Bending Schedule Essentials: Common Errors and Practical Insights for Civil Engineering should help your Knowledge in 2026

on

-

Read more: Recruitment Scams and the Promise of Reform in Govt of West Bengal 2026

Read more: Recruitment Scams and the Promise of Reform in Govt of West Bengal 2026Recruitment Scams and the Promise of Reform in Govt of West Bengal 2026

on

-

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

Read more: Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026Pile Foundation: The Hidden Strength Beneath Every Structure Now even in 2026

on

Frequently Asked Questions: Billing Process in Construction Projects

Q1. What is an RA bill in construction, and why is it cumulative?

A Running Account (RA) bill is a periodic payment claim raised by a contractor for work executed during a specific billing period. It is cumulative because each new RA bill shows the total work done from project commencement to the current billing date — not just the current period. The payment due is the incremental difference between the current bill’s cumulative total and the previous bill’s total. This cumulative format exists to ensure that any correction or re-measurement in a prior period is automatically captured and adjusted in the next bill.

Q2. What is the difference between an RA bill and a final bill in construction?

An RA bill is raised periodically during the project execution phase monthly or at milestones to claim payment for work done so far. A Final Bill is raised after the entire project scope is physically complete, all measurements are jointly finalized, all variation orders and extra items are settled, all quality certificates are in place, and all deductions are accounted for. The Final Bill closes the financial account of the contract and is accompanied by a No Claim Certificate (NCC) signed by both the contractor and the Engineer-in-Charge.

Q3. What documents must be submitted with an RA bill in Indian government projects?

The standard document set includes: the RA bill in the prescribed format (typically three originals for government projects), Measurement Book (MB) references with specific page numbers for all quantities claimed, GST Tax Invoice with the correct HSN/SAC code and rate, material test certificates for specification-controlled items (concrete cube reports, brick test results, bitumen test reports), dated and geotagged progress photographs, insurance certificates if contractually required, and labour attendance registers for labour-component contracts. For extra items, additionally: Technical Sanction order and Rate Analysis approval.

Q4. What is retention money in construction contracts, and when is it released?

Retention money is a percentage of each RA bill payment typically 5% withheld by the client as a financial guarantee against defective work or contractor default during the Defects Liability Period (DLP). It is withheld from every RA bill until the total retention pool reaches the contract’s maximum retention limit (often 5% of the contract value). After the DLP usually 12 months from the date of project completion retention is released following a formal DLP inspection and a written completion confirmation. In some contracts, the contractor may substitute retention money with a Bank Guarantee of equivalent value.

Q5. How does GST apply to the billing process in construction projects in India?

Construction services are generally taxable at 18% GST under HSN/SAC code 9954. Certain government civil works contracts and affordable housing projects qualifying under specific GST notifications attract a reduced rate of 12%. In government projects, the client entity deducts GST TDS at 2% under Section 51 of the CGST Act 2017 and deposits it directly with GSTN. The contractor must raise a valid GST Tax Invoice alongside every RA bill, with the correct rate, HSN/SAC code, and GSTIN details. In Maharashtra, compliance includes GSTR-1 filing, GSTR-3B reconciliation, and GSTIN registration for each project state.

Q6. What is the FIDIC equivalent of an RA bill?

Under FIDIC contracts primarily the Red Book (FIDIC Conditions of Contract for Construction) the equivalent of an RA bill is the Interim Payment Certificate (IPC). The contractor submits a monthly Payment Statement under Sub-Clause 14.3. The Engineer reviews it and issues the IPC within 28 days under Sub-Clause 14.6. Payment must be made within 56 days of the Payment Statement date under Sub-Clause 14.7. Unlike Indian government contracts where certification and payment timelines vary widely, FIDIC’s timelines are contractually binding and late payment automatically attracts financing charges under Sub-Clause 14.8.

Q7. What are the most common CAG audit objections in construction billing?

The most frequently encountered CAG audit objections in Indian construction project billing are: billing of incomplete or unverified work; excess quantities billed without a sanctioned deviation statement; extra items billed without Technical Sanction and approved rate analysis; non-deduction of BOCW Cess (1%); incorrect GST application; premature retention release without DLP inspection; inadequate or incomplete MB documentation; rates for extra items not supported by proper rate analysis; advance recovery gaps or delayed recovery; and billing of items not conforming to approved specifications.

Q8. What is a Technical Sanction, and why is it mandatory for extra items?

Technical Sanction (TS) is the formal written approval issued by the competent authority (typically the Superintending Engineer or Chief Engineer, depending on the financial limit) authorizing the execution and payment of work that falls outside the original sanctioned scope including extra items and significant quantity deviations. It is mandatory because billing a payment for unsanctioned work is a violation of financial propriety rules in government contracts and constitutes an unauthorized payment under audit standards. TS must always precede execution of extra items not follow it.

Q9. How is escalation calculated in construction contracts in India?

Price escalation (or Price Variation Clause PVC) in Indian construction contracts is calculated using a formula specified in the contract that links cost adjustments to changes in published indices. Typically, the formula assigns weightage percentages to labour, material, fuel, and other cost components. The variation in the relevant index (WPI for materials, CPI for labour) between the base date (usually the tender submission date) and the billing period determines the escalation amount. For example: Escalation = Paid Amount × [(Index (Current) − Index (Base)) / Index (Base)] × Applicable Component Weightage. The specific formula, indices, and weightages are always contract-specific.

Q10. What is a deviation statement in construction billing?

A deviation statement is the formal document that records and authorizes changes in quantities of BOQ items that exceed the originally tendered quantities by more than the permissible deviation limit typically ±25% in CPWD contracts, though the limit varies by contract. When the total executed quantity of a BOQ item is expected to vary significantly from the tendered quantity, a deviation statement must be prepared, submitted to the competent authority, and sanctioned before the deviated quantities are billed. Billing at quantities that exceed the BOQ without a sanctioned deviation statement is one of the highest-severity audit findings in Indian government projects.

Q11. What is Labour Welfare Cess, and who bears the responsibility for deducting it?

Labour Welfare Cess is a 1% levy imposed on the cost of construction under the Building and Other Construction Workers’ Welfare Cess Act, 1996. It is deducted from contractor payments by the client (government entity or private developer) and deposited with the State Building and Other Construction Workers’ Welfare Board. In Maharashtra, this is the Maharashtra Building and Other Construction Workers Welfare Board (MBOCWWB). The responsibility for deduction lies with the entity making the payment to the contractor, making it a mandatory recovery in every RA bill. Engineers who omit this deduction face audit objections and are personally accountable for the shortfall.

Q12. How should billing engineers handle disputed measurements in construction projects?

When there is a disagreement between the contractor’s claimed quantity and the engineer’s recorded measurement, the prescribed process is: first, a formal re-measurement is carried out jointly by both parties; second, the re-measurement is recorded in the MB with both parties’ signatures; third, if the dispute remains unresolved, the engineer records the quantity they are prepared to certify in the MB and the bill is processed for that amount; and fourth, the contractor’s objection is formally recorded, and the dispute is pursued through the contract’s dispute resolution mechanism, typically arbitration for government contracts and the DAAB for FIDIC contracts.

Conclusion: Why the Billing Process in Construction Projects Is Your Most Valuable Professional Skill

After years of working with billing systems, audit teams, contractor claims, and project financial reports, I have arrived at one clear conclusion: the civil engineer who understands the billing process in construction projects is always the most indispensable person in the room.

Not because billing is glamorous. It is not. It is meticulous, documentation-heavy, and often unglamorous work. But it is the work that keeps projects financially honest, contractors fairly paid, clients protected from cost leakage, and engineers safe from audit liability.

In India’s construction ecosystem with its unique blend of government tendering norms, GST compliance complexity, CAG audit rigour, BOCW welfare obligations, RERA-linked payment structures, and MMRDA/MCGM-specific requirements the gap between an engineer who understands billing and one who does not is enormous. And in the coming decade, as digital billing platforms, PMIS systems, and AI-assisted quantity verification become standard in large projects, the engineer who has internalized the principles not just the forms will lead the adoption curve rather than scramble to keep up.

This guide is the beginning of that journey, not the end. Every project you work on will teach you something that no blog can anticipate. What this guide gives you is the framework the process clarity, the audit awareness, the India-specific regulatory knowledge, and the professional discipline to approach every billing cycle with confidence.

Because when the auditors arrive and they always do the engineer who certified those bills should be able to look at every line with pride, not anxiety.

About the Author This guide is written by a Civil Billing Specialist with deep expertise in Indian construction contracts, RA bill preparation and certification, PMC-based project management, government project audit compliance, and FIDIC-based international contract frameworks. Based in Mumbai, the author works with civil engineers, contractors, and project management consultants across India to build billing systems that are accurate, audit-ready, and professionally sound.

The Conceptual Failure of Communism in West Bengal: How an Ideology Broke an Economy?

I want to start with a number that should haunt every Bengali who cares about…

Types of Foundation in Construction: A Complete Technical Guide for Your Positive Self Development

When I first started reviewing construction projects in Mumbai, I quickly realised that the one…

Billing Process in Construction Projects: The Complete Guide Every Civil Engineer Must Know & Improve in 2026

The Problem No One Talks About Openly If you have ever stood at a construction…

Basic Rate Difference of Aluminum Window Section from Ingot IE07: A Complete Guide to BRD Calculation, NALCO Rate Reference

If you are working in aluminum fabrication, construction procurement, or cost estimation, understanding the basic…

Self‑Healing Concrete (Bio‑Concrete): Concrete That Repairs Its Own Cracks

Why this topic matters in real projects? In most civil projects, concrete doesn’t fail suddenly—it…

The Ultimate Run Apocalypse: Why Teams Are Scoring So Heavily This IPL Season

The modern cricket landscape is witnessing a structural shift that has shattered historical data, outpaced…